Fall 2022 7 Exam Solutions On Competitive Strategy At The Michigan University

Why is there a reason for overall cost leadership?

Figure 3.4 is an example of an Experience Curve.

Figure 3.5 Economics of Scale

- Consumer demands have become more sophisticated and individual in many industries. The low-cost producer dedicated to producing a standard, no-frills product may find his customer base being whittled away by competitors adapting and developing their products.

- If the industry truly is commodity-based, then the risks of a low-cost strategy are great. This is because there can only be one cost leader, and if firms compete solely on price, being the second or third lowest cost producer confers little advantage.

| Illustration 3A

KWIK SAVE Supermarket success in the 1980s has been based on selling more products, more up-market, in bigger stores with more service. That messago has been driven home as Tesco and the others have followed Sainsbury's formula and Marks & Spencer's products. Gone are the price wars of the 1970s. The piles of cheap baked beans and the plastic daffodil special offers. Instead we have fresh, chilled, chicken-in-polythene complete with listeria and high prices. Tesco takes credit cards and has won prizes for its wines. Asda boasts crèches. The rules are clear. Make shopping exciting and you make money. Kwik Save breaks those rules with the glee of a delinquent schoolboy. And makes plenty of money doing so. Kwik Save sticks proudly to its highly unfashionable formula of selling limited ranges of branded groceries at lower prices than the rest, steering clear not just of fancy ideas such as delicatessens or in-store bakeries but also of any fresh produce. Cheap baked beans and breakfast cereals are its stock in trade- but only if they are Heinz, Kellogg's or the other market leaders. No own labels at Kwik Save. No nonsense about 'exclusive brands, as at Gateway. Initially, this was because the range was constrained by the policy of not pricing products. Sticking labels on every tin and packet costs a fortune in store labour. So Kwik Save opted for a unique approach of checkout staff memorizing the price of every item in the store - just like real grocers used to do. But that required the range be limited to 1.000 items, which also helped to keep costs down. Necessity was the mother of invention, then they made a virtue of necessity. The policy is being watered down now, since the computers linked to electronic scanning can remember rather more than a thousand prices. But even so, the range will be limited to 2,500 items even in the largest stores, and those largest stores are still much smaller than the football pitches being opened by the major chains. No frills' is the promise. 'No nonsense' is the motto. So far it seems to be working, and as people feel poorer from higher inflation and higher mortgage rates it ought to work better still. Because of its low overheads Kwik Save does not need the high sales and high margins achieved in the superstores. As chairman lan Howe commented: "We are happy for customers to come only three weeks out of four. They can buy their fancy food at fancy prices from the fancy stores of stars, so long as they shop at Kwik Save for the staples. The Guardian (1989) |

question:

what is the basis for a differentiation strategy?

answer:

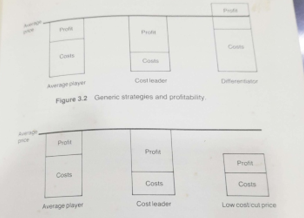

Just being different is not a differentiation strategy. Offering the industry's most unreliable and mechanically unsophisticated cars will not yield superior performance. The key to a successful differentiation strategy is to be unique in ways buyers value. If buyers are willing to pay for these unique features through higher prices, and if your costs are under control, the price premium should lead to higher profitability (see Figure 3.2).

Central to this strategy is an understanding of buyer needs. You need to know what the buyer values, deliver that particular bundle of attributes, and charge accordingly. If you are successful, then a subgroup of buyers in the marketplace (a segment) will not consider other firms' offerings as substitutes for your offering. You will have carved out a set of loyal customers, almost a mini-monopoly. This suggests that there may be several successful differentiators in a given industry. This is where the buyers can be segmented into distinct subgroups with particular requirements.

- If the basis upon which the firm seeks to be differentiated is easily imitated, other firms will be perceived as offering the same product or service. Then rivalry within the industry is likely to switch to price-based competition.

- Broad-based differentiators may be outmanoeuvred by specialist firms that target one particular segment.

- If the strategy is based on continual product innovation (to stay one jump ahead of the competition), the firm risks breaking expensive new ground merely for followers to exploit the benefits.

- If the firm ignores the costs of differentiating, the premium prices may not lead to superior profits.

The term "differentiation" is used widely in strategic management and marketing. However, it can be used loosely to describe a firm's positioning in an industry. In most industries, the firms do not offer precisely the same products or services as their competitors. For example, there may be differences in styling, the distribution channels used, and the degree of after-sales support. If these differences lead to a firm being able to charge premium prices (i.e. above the industry average), then the firm is differentiating, in Porter's terms. However, in many cases, these differences give us an idea of the particular firm's positioning in the industry.

Because there are few pure 'commodity'-type industries, most firms in most industries inevitably have to offer something slightly different to be in the game. These firms would only be differentiators if they could charge premium prices. This point is taken up again at the end of this chapter.

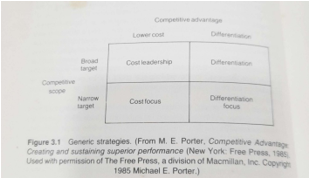

Focus

So, firms can compete on a broad front (serving many segments) or on a narrow front (focusing). Both variants of the focus strategy rest on differences between the target segments and other segments in the industry. These differences result in the segment being poorly served by the broad-scope competitor, which needs to be better equipped to tailor its offerings to its particular needs.

Broad scope differentiation and focus differentiation are often confused. The difference between them is that the overall, broad scope differentiator bases its strategy on widely valued attributes (e.g. IBM in computers), while the focus differentiator looks for segments with special needs and meets them better. (see Illustration 3B 'Apollo Computers')

| Illustration 3B

APOLLO COMPUTERS Companies like Apollo don't oporate in markets defined by mass volume production, standardization of commodities and intense price competition. Apollo makes 80 systems daily, which are grouped in five families with 200 variables in each. They cost around £26,000. They field their highly specialized commodities in targeted, segmented markets, with sophisticated sales teams. And instead of heavy-duty layers of management and rigid enforcement of the separation of conception and execution, they cultivate their workers' commitment to their commodities. The company also unifies the workforce by designating everyone staff, sponsoring higher education, offering the same holidays (25 days) to everyone, providing free cancer screening, a smart gym on site and private health insurance. It has compressed the management structure, and assembly staff travel along the line with the computer they are making. A faulty product goes back to its producer. That generates its own discipline. 'We're all quality managers." The Guardian (16 August 1989). |

Either someone else comes in, 'out focuses' you, and steals your buyers, or the target segment withers away for different reasons (e.g. changing tastes, demographic shifts). However, there is an attraction to the idea of targeting a narrow segment and tailoring your offering accordingly. If you get it right, it makes for a good business. But, if you were once a broad-scope player and decided to target the higher value-added segments solely with a differentiation focus strategy, some nasty surprises may lurk.

If you have spotted the benefits of trading up and targeting, you can be sure that others have seen the light too. Before you know it, those price-insensitive, high-end customers will have plenty of firms to choose from, ending your price premium. As well as being attacked from the pricing side, there may be problems with cost levels in store. So you could be squeezed from both the price and cost directions.

question:

Assess the generic strategy concept

answer:

Porter's contribution has been invaluable. He has raised the level of debate about strategy substantially. However, this concept of generic strategies is not without its problems. We have noted above that the cost leadership strategy requires the firm to match the industry's average quality.

| Illustration 3C

A NEW YEAR FIRE SALE? Barkers plead with passers-by to enter Abraham & Strauss' new store in mid-town Manhattan, to apply for a charge card and spend, spend, spend. The desperation is understandable, and not just because A&S is the first big department store to open in New York for more than twenty years. Many of America's most famous stores - A&S, Bloomingdale's, Marshall Field and Sears, Roebuck among them - face the biggest upheaval in their history. The challenge for each is to find a retailing role that it can perform better than anybody else. Those that lack a clear purpose and identity, as Gimbels did, will go out of business. All of America's department stores are caught in a vice: on one side they are squeezed by speciality stores offering customers more choice and lower prices (such as Toys 'R' Us and Radio Shack, a chain specializing in electronics), and on the other by discount stores and European-style hypermarkets with scant service but unbeatable prices. The squeeze is tightened for some department stores by huge debts amassed in leveraged buy-outs. Both Macy's and Marshall Field have deliberately moved out of the market for cheap merchandise, leaving it to the discount stores. Sears, Roebuck's role as an updated version of the nineteenth-century general store-selling reliable but unstylish clothes and goods - looks increasingly antiquated. Speciality stores are luring away customers from even its renowned hardware departments. Sears' share of the paint market has declined from 42 to 18 per cent; of the appliance market from 46 to 32 per cent. Several other stores have retreated from such unprofitable lines. A&S has only token furniture and electronics departments in its new flagship store in Manhattan; Macy's has all but conceded the camera market to specialist stores. Sears still tries to do everything and so does nothing very well. Its profits are stuck in a rut and it risks, like F.W. Woolworth, becoming yesterday's store. J.C. Penney, once a near copy of Sears, has a much clearer direction in opting to become more like the American equivalent of Marks & Spencer. It is concentrating on fashionable, mid-market clothes, especially women's wear, and abandoning such relatively unprofitable lines as hardware and electronics. The Economist (7 October 1989). JAPAN INC. - STUCK IN THE MIDDLE? The strategic positioning that has served Japan so well in the past is no longer tenable. On the one side, there are German companies like Mercedes and BMW commanding such high prices that even elevated cost levels do not greatly hurt profitability. On the other are the low-price, high-volume producers like Korea's Hyundai, Samsung and Lucky Goldstar who can make products for less than half of what it cost the Japanese. The Japanese are being caught in the middle they are able neither to command the immense margins of the Germans nor to undercut the rock-bottom wages of the Koreans. The result is a painful squeeze. Kenichi Ohmae, McKinsey Tokyo, 1987. |

This is not a 'cheap and cheerful' option. If the product is considered substandard, then low prices would be required to sell it, thus eroding the profit margin. Similarly, we noted that the successful differentiator needs to think about costs. In particular, this firm must be ruthless about paring costs that do not feed through into something valued by the buyer.

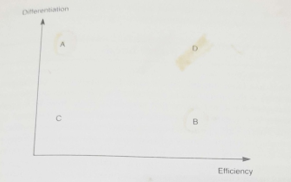

So, whereas at first sight, these two strategies might seem to be distinct and mutually exclusive, on closer inspection, they appear to have strong common elements: both require a high concern for quality (especially as one route to low costs is to eliminate scrap and reworking), and they both require close attention to cost control. If this is the case, it might be useful to consider these two not as exclusive alternatives but as orientations (see Figure 3.6).

A firm in position A in the figure would pursue an uncompromising differentiation strategy, serving a particular segment with a unique blend of product/service attributes and earning a premium price. There is no great attention being paid to achieving efficiency. Most of the management time and effort is devoted to preserving and developing those strengths that have led to success, be it constant product innovation, unrivalled quality, or rapid response to customer requirements.

The firm in position B is pursuing a 'pure' efficiency strategy. Efforts are channelled into driving costs down across the whole organization. There is little attention devoted to product/service development. Superior profits come from low costs matched with average prices.

The firm in position C is pursuing neither efficiency nor differentiation. It is Porter's 'stuck in the middle firm. A lack of differentiation means no opportunity to raise prices above the industry average, and below-average efficiency leads to above-average costs. So, firms in position C are squeezed from both ends.

The firm in the enviable situation of position D has the advantages of both strategic orientations. The firm's ability to differentiate success fully leads to premium prices, while efficiency yields cost advantages. Firms in position D will therefore outperform others in the industry. Achieving both sources of advantage at the same time is difficult. Usually, differentiation requires adding features that add to costs; achieving the lowest cost position in the industry requires the firm to give up some differentiation by standardizing the product. But the greatest difficulties derive from the inconsistent and often conflicting demands on the organization that each strategy makes. We look into these differing requirements in the next chapter.

Figure 3.6 Differentiation and Efficiency

question:

what are the problems with Porter's generic strategies?

answer:

- Why must you be the lowest-cost producer in the industry? Surely, being second or third lowest would still yield above-average profits? Porter's argument rests on the links between sales volume and achieving the lowest costs. If there is a strong experience curve effect in the industry, or if economies of scale can be achieved only where one firm has a significant market share, then if two or more firms are seeking the low-cost position, a full-scale price war is likely to result. The only winner would be the lowest-cost producer. But, if these experience and scale effects do not operate to any significant degree. And if the firms in the industry compete on many non-price dimensions (like service, advertising, and distribution channels), the disadvantages of being the second or third lowest cost disappear.

- There are other exceptions to the 'rule that firms must choose either one or the other generic strategy Innovation (especially innovation in production processes) can help firms slash costs and differentiate simultaneously. Also, if cost is closely linked to market share, then the low-cost market leader may be able to enhance its ability to differentiate and still be the lowest-cost producer. Alternatively, the successful differentiator may find itself with the sales volumes to enable it to become the cost leader (e.g. where the firm differentiates through establishing strong brands).

Buyer needs

What has been missing so far from this discussion of competitive strategy is the buyer and, in particular, the buyer's needs. None of the strategies discussed above will succeed unless a group of buyers wants the particular bundle of attributes offered by the firm. There is little point in pursuing an extremely low-cost position in manufacturing mechanical calculators if no one wants them anymore. This is an extreme example, but it emphasizes that successful strategies must start with understanding buyer needs. Buyer needs change, as we saw in Chapter 2, so successful firms must continually keep in touch with their customer's needs and anticipate how they may change. Taking this line of argument further, when we are trying to define the firms in our 'industry. The customer's perspective is the most reliable (and useful) starting point. The customer's (or potential customer's) perceptions of alternative providers of products/services that meet their needs might be rather different from the firm's perceptions of its competitors.

I'm convinced that the winners in financial services will be the ones that pay the closest attention to the customer. That means I must say first, second, and third, what does the customer want? (Peter Ellwood, chief executive of TSB's retail banking)

question:

Assess the Illustration 3D list ideas about buyers

answer:

As industries evolve, the nature of competition changes. 'First mover advantages gained by early adopters of an innovation are rapidly reduced as other firms follow suit. For example, in chartered accountancy, firms started to explore how they might add value to their basic audit service (e.g. by offering business advice to their clients). Soon after the leading firms began implementing this strategic move, others jumped onto the bandwagon. The game's rules have changed; what was once a key feature of a successful differentiation strategy now becomes the norm.

As consumers become wealthier and more accustomed to quality, reliability, and innovation, the standards in many industries are continually being raised; for example, in the early 1980s, only one or two car manufacturers offered anti-corrosion warranties (8, Volks Wagen/Audi).

Illustration 3D

UNDERSTANDING WHAT THE CUSTOMER REALLY WANTS

Do you know:

This information about buying influences must permeate every part of the business.

Some techniques

Shops 'neglect service' Mintel, commissioning researcher of the survey of 1,430 adults, suggests that the big chains have been so preoccupied with matching each other's prices and products that failings in staff training and after-sales service have gone unnoticed.

Only now, with customers complaining that there is too little to distinguish shops, are retailers likely to look for something else that can give a them competitive edge.

Given the investment by some big retailers in the campaign for Sunday opening. It was significant that the 18 per cent of customers who considered legislation crucial were outnumbered by those interested in children's play areas, baby changing rooms and toilets, and packers at checkouts. Faster supermarket checkouts were the main concern of 47 per cent of the sample. Fifty-nine per cent thought the introduction of knowledgeable staff offering 'real help would be a key advance in shops selling electrical goods. This also came top of furniture store customers' improvement list and they also regarded speedy home deliveries at a time which suited them rather than the van driver as important.

Shoe-shoppers were particularly irritated at being pressed to match with extras such as polish. One in four customers said rival shops sold the same style of shoes.

Caroline Dunn, senior analyst, says that the unique Ingredient of shops ought to be the way they treat the consumer: All our research points towards a lack of awareness of the different stores, especially in the footwear, electrical and do-it-yourself sectors because they are so much the same. In our view, it is through levels of service that they can differentiate themselves. Sunday Correspondent (24 September 1989). |

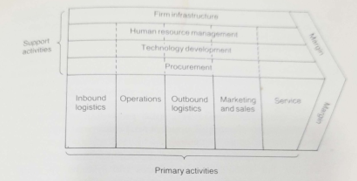

Figure 3.7 The Value Chain

Value activities can be divided into two broad types: primary activities and support activities. Primary activities are those that are involved in the physical creation of the product or service, its transfer to the buyer, and any after-sales service.

question:

explain the categories of primary activities

answer:

- Inbound logistics. Activities associated with the receiving, storing, and dissemination of inputs to the product (including warehousing, inventory control, and vehicle scheduling).

- Operations. Activities associated with transforming inputs into the final product (machining, packing, assembly, testing, equipment maintenance).

- Outbound logistics. Collecting, storing, and distributing the product to buyers.

- Marketing and sales. Activities associated with providing a means by which buyers can purchase the product and inducing them to do so (advertising, selling, channel selection, pricing, promotion).

- Service providing a service to maintain or enhance the product's value (installation, training, parts supply, repair, and maintenance).

Each of these may be a source of advantage, and, depending on the industry, different activities will be emphasized (e.g. in the photocopier industry, service is critical).

question:

explain the categories of Support activities

answer:

- Procurement. This is the function of purchasing inputs. It includes all the procedures for dealing with suppliers. Procurement activity goes on across the whole firm; it is not just limited to the purchasing department. Although the costs of procurement activity form only a small proportion of overhead costs, the impact of poor procurement can be dramatic, leading to higher costs and poor quality.

- Technology development. This embraces not just machines and processes but 'know-how', procedures, and systems. In some industries (like oil refining), process technology can be a key source of advantage.]

- Human resource management. This includes all the activities involved in staff recruitment, training, development, and remuneration. Some firms recognize the potential advantage gained through coordinating these activities and investing heavily in them (e.g. IBM, Unilever). The recruitment and retention of good staff have emerged as a major strategic issue for firms like chartered accountants and engineering contractors.

- Firm infrastructure. This includes general management, finance, planning, estate management, and quality assurance. The infrastructure supports the entire value chain (unlike the other three support activities, which can be particularly linked with one or two primary activities). The infrastructure can help or hinder the achievement of competitive advantage. An excellent management information system can help to control costs; a rigid departmental structure can hinder communication across the organization which may impede product innovation.

Links between the firm's and the buyer's value chains can be important sources of either cost reduction or differentiation. If the firm is supplying products or services to another firm (rather than the final customer), it is worthwhile to construct a value chain for the buyers' organization. The more we understand our customer's business, the better we can demonstrate how we can help them enhance their performance.) By tuning into the buyer's business needs better than our competitors, we can set up linkages with our buyers that make it costly for them to shift their business away from us. These switching costs can be real, tangible, or perceived inconveniences.

The value chain can also be useful in helping distinguish between the things we do that help to differentiate and those features of our product/service that are merely different. For example, many computer manufacturers have invested heavily in speeding up their microcomputers so that processing speed has become a basis for competing in the industry. But is speed valued by all customers? It is, presumably, important for some buyers but may be irrelevant for others. The value chain can help us analyze the buyers' needs so we can make better judgments about what the buyer values, and it can help us see where the costs of differentiation are in our firm. This could help us decide where we might trim out costly features, not particular customer groups do not highly value.

We explore the organizational implications of various strategies in the next chapter.

Positioning the firm

This section links together three themes that have been explored so far:

- The firm's industry structure,

- The needs of the customer.

- Generic strategies.

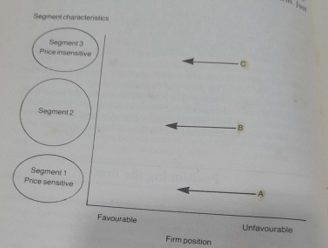

The vertical axis of Figure 3.8 refers to the characteristics of a customer group or segment. Three broad segments are indicated in the diagram:

Segment 1 People in this segment demand a standard product, and they are very price sensitive.

Segment 2 These customers want something different from the basic 'commodity' demanded by segment 1. Customers in segment 2 are less price sensitive than those in segment 1 and are prepared to pay more to the firm that can tailor its products/services to meet their particular requirements.

Segment 3 This group is prepared to pay for uniqueness, innovation, and exclusiveness. They are (almost) insensitive to price.

The horizontal axis in Figure 3.8 refers to the firm's position in its industry. This extends the ideas about analyzing industry attractiveness developed in Chapter 2 to the situation of an individual firm.

Figure 3.8 Positioning the Firm

As we can determine the relative attractiveness of a whole industry, we can use the same categories (the five forces) to assess the position of a firm within that industry.

A favourable position for a firm would be one where most of the following conditions are obtained:

- The firm has loyal customers.

- Suppliers are not in a position to restrict supply or bid up prices.

- Other firms within the industry (or from outside the industry) find it difficult to poach the firm's customers.

- The firm has low costs relative to other firms in the industry.

Unfavourably positioned firms would not enjoy these conditions; they would be susceptible to threats from other firms, suppliers, and customers.

A shorthand way of looking at industry position is to consider the firm as having its barriers to entry. These can be strengthened by improving the firm's relative cost position.

Firm A in Figure 3.8 has a poor industry position and is currently serving a price-sensitive segment) How can this firm improve its position? It may be that an analysis of the industry as a whole reveals that the prospects for this industry are most unattractive (due to, say, powerful buyers, declining demand, the strong threat from substitutes, etc.). In this case, there may be an argument for this firm to get out of this industry. (This begs the question of what industry the firm could profitably compete in. Answers may be thin on the ground.) Assuming that the underlying structure of the industry is sound, there would appear to be two basic options open to the firm:

- Improve its position by ruthlessly cutting costs. This would enable the firm to overcome pressures from suppliers' cost increases and buyers' demands for lower prices. If the firm could reach the position of cost leader, it might be able to compete on price, drive out some higher-cost players and improve its position accordingly. One problem with this strategy is that the low-cost position may be strongly linked to market share (due to scale or experience curve effects), but when serving this segment, you need to cut the price to get sales volume. If you lose this battle for market share, you will likely go out of business. So Porter's cost leadership strategy would appear to be relevant here.

- Try to lock in a subgroup of customers. This would be feasible if a group of Customers wanted something different. These differences could be due to geographical location access to distribution channels or particular requirements like, for instance, needing delivery in bulk. Targeting this subgroup may not get you premium prices (so this is not a pure differentiation strategy in Porter's terms), but it may help you to set up re-switching costs for your buyers. This would help to protect at lea a part of the firm's customer base from attack. This is analogous s Porter's cost focuser.

Firm B, in Figure 3.8, could try to differentiate by tailoring its products or services more closely to the requirements of a particular customer group. However, the price premiums available here are not likely to be great. Therefore, firms serving this middle ground of consumers need to pay great attention to efficiency. Large sales volumes may be needed to spread overheads. This may then mean that many subgroups need to be served, which, in turn, would restrict the firm's ability to focus exclusively on the needs of each subgroup.

Firms facing these broad segments need to offer something different to secure their position in the market, but this is not the same as Porter's differentiation strategy because only very modest price premiums can be charged. Are these firms able to pursue cost leadership? Maybe they can, but by definition, as there can be only one cost leader, this would seem risky.

So are these firms destined to be 'stuck in the middle? Possibly not because there are benefits from improving efficiency even if the firm does not become the lowest-cost producer in the industry. The risks of not being the lowest-cost firm are much reduced here because the customers are not concerned only about price, and firms looking for efficiency would probably avoid getting into a price war. So these 'middle ground' firms would try to position themselves differently to secure or increase sales volumes rather than to seek premium prices.

Firms facing price-insensitive segments (firm C in Figure 3.5) need to emphasize strongly those features of the product/service that are most sought after by these buyers. Innovation or quality must come with fine cost control, and efficiency improvements take a lower priority. This way, firm C can strengthen its position by setting up high real or intangible customer switching costs. This can be done through branding, tailoring the product, and establishing links and dependencies between the firm and the customer.

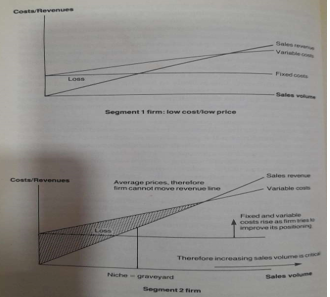

In Figure 3.9, we have used the breakeven chart to simplify the strategies of firms facing these three customer segments. The low-cost/low-price firm serving segment 1 has low fixed and variable costs. This enables it to price competitively and profit at relatively low sales volumes. However, if the prevailing technology in this industry meant that there were significant scale economies to be had with large, automated production processes, then firms adopting this technology would have high fixed costs (but probably even lower variable costs). Consequently, they would need much greater sales volumes before they broke even.

Firms serving segment 2 must invest more than segment 1 to be different. This is likely to load up both fixed and variable costs. They will need high sales volumes to spread these extra costs if they cannot charge a premium price for these different offerings. The danger of carving out a niche too narrowly in this segment is clear.

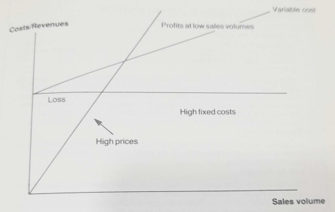

Segment 3 customers are relatively price insensitive. They are prepared to pay for the added quality the successful differentiators offer. Depending on the particular cost structure of the firm and the extent to which customers will tolerate high prices, firms serving segment 3 can afford to carve out market niches. We could go further and suggest that without focusing, a firm would not easily be able to sustain its position in this exclusive market.

If we take the airline industry over the North Atlantic as an example, our three segments might be:

Segment 1 These customers are looking for the cheapest way to cross the Atlantic. They are prepared to forgo flights at their convenience and in-flight comforts if the price is low Students might fall into this segment. These are the majority of business and leisure passengers.

Segment 2 who are looking for a little more comfort and convenience and is willing to pay above the basic price to get them.

Segment 3 VIPs value flights at their convenience, speedy ground service, exclusivity, and luxurious in-flight service.

Segment I would be well served by the 'pack 'em in' charter operator, operating out of marginal airports (to avoid costly landing and handling charges) and offering minimum in-flight service (bring your lunch). All frills have been stripped out to achieve low costs and low prices.

Figure 3.9 Breakeven-charts

Segment 3 firm: Successfully Differentiating

Figure 3.9 Contd

Segment 2 is large, and within this broad grouping, there may be opportunities to identify subsegments with particular needs. However, we have said that these passengers are only prepared to pay a modest premium over the basic price. Airlines serving this segment must attract sufficient passenger volumes to cover additional costs. Attempts at differentiation add to these costs (see Illustration 3E 'Desperately seeking differentiation).

Segment 3 passengers could be served in several ways. They may be attracted to the first-class cabin of a regularly scheduled flight (but they still have to mix with the tourist class, so this would not suit all. of them). Or they may prefer to charter their executive jet. Better still, why not buy one?