Solved Supply Shocks Exam Questions for Your Revision and Success

We’ve shared high-quality answers to questions that help our readers write their next supply shocks exams with more understanding and confidence. Please don’t hesitate to use the solutions for your revision, too. All are free to view.

Analyze The Thatcher Miracle in Light of Supply Shocks and Growth

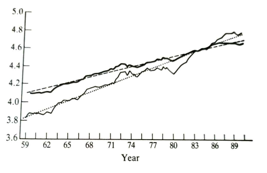

During 1980 considerable attention was paid to manufacturing productivity (output p head). The government was not slow to publicize the figures, but other commentators also recognized that something peculiar seemed to happen. Figure 12.3 tells an interesting story. The chart shows h productivity has risen since 1959, for the manufacturing sector and the whole economy. It also shows the estimated trends.

Figure 12.3 Productivity for manufacturing and the whole economy

(log scale): ------ whole economy, ------- manufacturing, ------- manufacturing trend, ---------whole economy trend.

The figures for the whole economy show no evidence of a productivity miracle. Indeed, the period from 1979 to 1991 is scarcely better than the post-oil shock period, despite the substantial contribution to GDP from oil production.

So, the case for a miracle rest in manufacturing. The chart is drawn with a log scale, which lets us see immediately the rate of growth of productivity. which is the slope of the line. The chart, like UK economic history, can be divided into three periods. The first is from 1959 to the 1973 oil crisis, the second from 1973 to 1979, and the last from 1979 onwards. The latter period can be thought of as the Thatcher decade. Table 12.1 gives the key figures. They should not be taken too literally, as productivity growth (like output) is sensitive to the cycle, but they do give a broad picture.

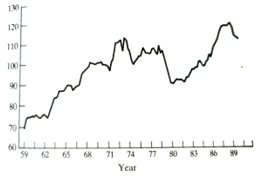

The basic picture for manufacturing is of moderately high growth in the 1960s and 1980s, and a moribund period in the 1970s. The figure shows that there was a period of exceptional productivity growth in the 1980s; between the last quarter of 1980 and 1986, productivity grew at an annualized rate of 6.1 percent. However, as Figure 12.4 reveals, this surge was coincident with what turned out to be an unsustainably rapid recovery in manufacturing output from the very severe slump in 1980.

Figure 12.4 Manufacturing output (1985-100).

Table 12.1 Productivity growth rates (annualized percentages).

Percentage Growth Rates

| Period | Whole Economy | Manufacturing |

| 1960Q1-1991Q3 | 1.9 | 2.9 |

| 196001-1973Q1 | 2.5 | 3.4 |

| 1973Q2-1979Q2 | 1.2 | 1.0 |

| 1979Q2-1991Q3 | 1.4 | 3.3 |

Why Did the Growth Rate of Manufacturing Productivity Rise?

The most profound is technical progress. This can encompass progress in management and organization, as well as the invention of new processes. We relegate the discussion of the broader determinants of this to the next section; but disregarding the causes, the empirical question of whether this actually occurred in the period in question is really the issue we seek to resolve here.

Second, and more mundanely, any apparent effect may be a purely statistical artifact, due to measurement problems, or the relative decline of low-productivity sectors as unproductive firms go out of business (which will tend to raise average productivity). While this argument is plausible and had many adherents among anti-government commentators in the 1980s, this was not in fact the case in the United Kingdom: see Layard and Nickell (1989).

Third, productivity will rise if the capital stock grows. While there has been positive net investment in the manufacturing sector since 1979, it is manifestly not the case that there has been an unusual rise. Indeed, as we saw above there is plenty of evidence that the capital stock fell in the early 1980s, although this is not picked up by the official CSO measure.

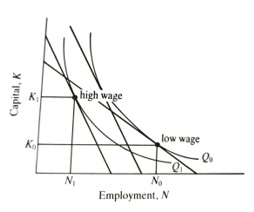

Figure 12.5 The optimal capital/labor ratio.

A more subtle explanation is that the capital-to-labor ratio has increased. Figure 12.5 shows the quantities of capital and labor required to produce a fixed level of output Q. The optimal point on any isoquant is determined by the relative price of capital and labor. From basic theory, as the relative price of labor rises, the firm will slide along the isoquant while the optimal supply of output will fall (from Qo to Q1). Thus (in this case) the response to a rise in wages is to raise the capital stock only slightly but to raise the capital-to-labor ratio much more dramatically. The effect comes not from a rise in capital stock but a fall in employment. This explanation is rather plausible for the United Kingdom.

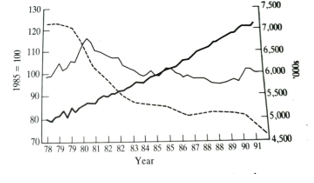

Figure 12.6: Manufacturing employment and real wages:

------real earnings, ------employment, --------real unit labor costs.

Figure 12.6 shows how real wages and manufacturing employment moved from late 1970 The rise in real wages and the fall in employment after 1979 are both equally marked, although there are clearly other factors involved. The remarkable phenomenon is that the unprecedented fall in demand around 1980 had apparently no effect on real wages. As we have seen, output fell because the real exchange rate rose, choking off the demand for exports and reducing the demand for domestic production as imports became relatively cheaper. This contraction in demand necessitated a fall in real wages in order to maintain competitiveness, but this did not occur. As output slumped, productivity fell, pushing up real unit labor costs. The rise in unit labor costs mirrors a fall in profitability: firms responded by shedding labor, increasing productivity so that real unit labor costs fell again. As the exchange rate fell, output was able to rise again in the mid-1980s and the fall in employment returned to its long-run trend. However, the substantial rise in the level of real wages left a permanent residue in the form of a higher capital to labor ratio. Of course, this begs the question of why real wages were so stubbornly immune to the effects of recession.

The explanation offered here seems to explain the bulk of the productivity rise; the econometric evidence is quite consistent with this story, as research at the National Institute reveals (Financial Times, 25 October 1989). However, many people close to the industrial ground fervently believe that there has been a shake-up in industrial relations and management practices in the United Kingdom.

The anecdotal evidence for this hypothesis is very convincing. Many studies report that work practices now make for more flexibility, and therefore efficiency, than ever before see Cross (1988a), for example. Industrial relations have clearly improved in quantifiable respects - the level of strikes in 1991 was the lowest for a century on some measures. It is quite likely that without this shift in attitudes and practice the move to a higher capital intensity could never have taken place on the scale that was needed; but this shift may well prove to have been a one-off boost to productivity, rather than a source of continuing productivity increases.

Nevertheless, it is worth considering why this organizational change came about. Essentially, there are two candidates for the explanation: first, the reduction in union power engendered by Mrs. Thatcher's union reforms, and second the massive shock to the industry in the early 1980s. The anti-union legislation weakened the capacity of unions to resist changes in their work practices, while the latter effect provided a stick of unprecedented size with which to encourage management to push through change and unions to accept it. A popular argument for the poor long-run performance of the United Kingdom economy is that the UK has been spared the major shake-ups that have struck most other, faster-growing countries. The 1980-81 recession provided just such a shake-up. Layard and Nickell (1989) quote the chairman of a large manufacturing company as saying: "Both management and workers looked over the edge of the pit and stepped back.

Discuss The UK’s Long-Run Growth in Light of Supply Shocks and Growth

The last section examined whether an increase in the trend growth rate of productivity occurred in the 1980s: the conclusion was, probably not. The reason why this issue has such potency is that the growth rate of the UK economy has been the subject of intense study and interest for decades. In a sense, growth is the major macroeconomic issue; in the long run, it dominates everything else. In the end, most economic shortcomings will be forgiven if growth is high; certainly inflation, and probably also unemployment, and this matters. In 1870 Britain had a GDP per capita that was about 25 percent greater than the United States and five times that of Japan (Feinstein, 1988). By 1984, after 114 years of relatively low growth, the United Kingdom was only 70 percent as productive as the United States and 90 percent of Japan. In one sense this is the single most important topic that observers of the British economy should be examining.

In light of this discussion, it may appear remarkable that one of the major engines of growth has largely been ignored by the economics profession. Robert Solow (1957) showed how growth can be 'accounted for by the sum of three factors: growth in the labor force (which is more or less exogenous), growth in the capital stock via investment, and finally technical progress. Estimates vary, but it soon became clear that a substantial component of economic growth must be ascribed to the latter effect; Solow thought about 90 percent for the United States, although later estimates put this nearer 50 percent (Kendricks, 1973). However, the response of the economics profession was in large part literally to ignore the effect; technological progress was measured as the 'Solow Residual" - the bit of output growth left over when growth in capital and labor had been stripped out. This does not mean that growth was ignored. Considerable effort has been put into determining the rate of capital accumulation. This process began at least a hundred years ago; Marx's opus was entitled 'Capital', after all. In the neoclassical tradition, the basic framework was established in the 1950s by Solow (1956) and Swan (1956).

Gradually, this asymmetric approach to growth theory began to seem more and more unsatisfactory. Quite apart from the intellectual problem, there was an apparent empirical problem with the standard neoclassical model. If the state of technological progress is simply an exogenous lump available to all, to be gathered out of thin air as it were, then poor countries differ from rich ones only by virtue of having less capital. By diminishing returns, this implies that the return on investment is higher in poor countries, and the theory predicts that their growth should be correspondingly higher. So poor countries should 'catch up' with the rich; there should be convergence in international income levels. The problem with the theory is that while there is some evidence of convergence among industrial countries, there are really very few signs of convergence where one would most expect it - between developing and developed countries. Indeed, the world seems to be categorizable into 'growth clubs', within which convergence occurs, but not between; see Dowrick and Gemmell (1991) for some evidence on these issues. The decline of Britain is another piece of evidence. What should have happened is that the rest of the world caught up with us not, as actually happened, overtook. There are two main stories of endogenous growth," both of which revolve around the notion that knowledge is crucial to the production process. The of these was introduced by the Nobel prize-winning theorist Kenneth Arrow in 1962, but his idea lay largely moribund until Romer revived it in 1986. Arrow's insight was that agents learn by doing. This notion, well established in nitty-gritty studies of industrial organization, holds that the more you do something, the more efficient you become: productivity is positively related to experience. Moreover, this productivity bonus is to some extent a shared resource; how to do things becomes common knowledge. The significance of this is that there are external benefits to growth, as the pool of experience is available to all. As usual, the existence of an externality leads to inefficiency. Competitive economies will grow too slowly in these circumstances. Note that with constant returns to physical factors, the additional intangible factor of production (knowledge) implies there are increasing returns to scale. Normally, this would be inconsistent with perfect competition (as the size of firms is unbounded), but as the returns operate through an externality, each firm alone acts as if there are constant returns. Romer's variant on this basic model was to allow knowledge to exhibit increasing marginal productivity, although the production of knowledge - via investment expenditures on research and development - possesses conventional diminishing returns. The significance of increasing returns to knowledge is that it allows us to step away from Arrow's model which possesses a unique steady state, albeit inefficient, to a multiplicity of endogenous growth paths. The intriguing possibility emerges of capital flows from poor to rich countries, seeking higher rates of return.

The second story puts the emphasis on knowledge embodied in people. A human capital-intensive research sector of the economy produces ideas, which enhance productivity. These ideas are embodied in the production process, and also add to the stock of existing knowledge, thus increasing the productivity of the research sector. These ideas can be traced back to Uzawa (1965), but it was Robert Lucas (1988) who reintroduced them in a modern context. As in the Romer model, there is an important externality, which could provide a strong argument for public subsidy in education and research.

What Are the Policy Implications of The Theories Above?

The policy implications of these theories are fairly clear. In the learning-by-doing case, growth feeds on growth; there should be a kind of multiplier effect following growth. Fast-growing economies will tend to maintain growth or indeed accelerate. The human capital tale justifies subsidies to education, training and research as a response to the knowledge externality. So far as Britain is concerned, the explanation for our low growth could lie in the vicious learning-by-doing cycle whereby low growth perpetuates itself, or in our education and research sector. Although the share of research in relation to GDP in the United Kingdom is of a comparable order to other countries, it is skewed towards defense, a relatively unproductive area. For example, in 1960 the air industry export market was one-quarter the size of the chemicals market, but 35 percent of all research and development expenditure was in aerospace. By contrast, Germany devoted 33 percent of its expenditures to the chemical industry. It is also well established that although the United Kingdom has an elite educational system second to none in the world, it fails to educate the average citizen as well as in other industrialized countries. It is obviously difficult to make formal comparisons in some subjects, but in mathematics standard attainment tests are easily available. Sig Prais at the National Institute of Economic and Social Research (NIESR) has made many studies of comparative attainment in different countries. The most recent review of his and others' findings is given in Green and Steedman (1993) One of his findings is that the average UK schoolchild in secondary education lagged no less than 18 months behind their German counterpart the average German 12-year-old performed as well as the average British 14-year-old. In France, 66 percent of 16-year-olds have qualifications equivalent to GCSE grade A-C mathematics; in Germany, the figure is 62 percent, but in England, it is a mere 27 percent. In the field of vocational training, France and Germany awarded 98,000 and 134,000 mechanical and engineering qualifications in 1987; in Britain, the figure was 30,000. The typical British worker is poorly educated and badly qualified.

Plausible as the policy prescriptions of the new theories are, as yet it is unclear to what extent they hold. Testing the models is, in their very nature, very difficult. We need to identify a specific factor-for example, the human capital knowledge base - and find a measure of it. The example makes it obvious how difficult this is likely to be. As yet, convincing evidence for the new theories is yet to arrive. Unfortunately, given the profundity of the implications, if the models are true, this does not mean we can ignore the problem.