Spring 2022 Semester Exam Solutions For The Corporate Planning Process At Newcastle University

What does organizing a corporate planning process involve?

What circumstances might lead to the failure of planning?

- When the chief executive allows no one but himself to make decisions, there are many companies like this, and their size is a function of the ability of the one man who runs them. They are unlikely to be of great size and, without some change in policy (or a new chief executive of the same kind), will die with the entrepreneur who leads them. Successful or unsuccessful, they will all be unable to use the discipline of corporate planning-if only because it is a discipline with a formal approach.

- The small company cannot afford the time needed to write down plans so straightforwardly that all the major implications can be carried in the chief executive's head. The very small companies that do not employ an accountant of their own would be wasting their money if they moved into a more sophisticated management area. While small, they can only be very successful with formal planning and have a high probability of remaining small.

- The company is sinking so rapidly that it requires all those on board to operate the pumps. Until it can get the holes caulked and the ship floating, it has very little prospect of formalizing its planning process. Such a company may, of course, wish it had introduced corporate planning many years ago and avoided the situation in which it now finds itself.

Outline the objections to formal planning

What is a long-range plan?

State and explain the types of corporate plans

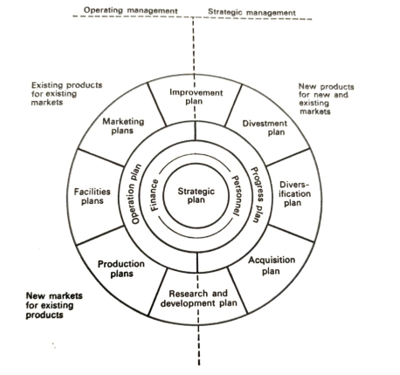

Fig. 1 Generalized planning system

At this stage, I must confess that the word plan still tends to suggest an image of a huge leather-bound document, perpetually locked and hidden deep in the company archives. I do not think I am alone in this--for example, I once had a perfectly serious inquiry from an acquaintance who wanted to know what a strategic plan looked like and how long it was. "Plan" must not be interpreted in such a way in the conceptual approach I have outlined (no corporate plan should ever gather dust in the archives!), and in many cases, the whole "plan" may be only a few sheets of paper. Sometimes, it may be long enough to make up a file or a book. The objective should, of course, be to keep plans as concise as possible, but at the same time, they must include enough data to make them actionable. There is some merit in having the various parts of the total package so that they can be lifted from the whole because of their confidential nature; it may be advisable to restrict readership of the total corporate plan. In this case, various sub-plans may be taken from the whole and passed to those who must act on them.

The total approach discussed above is for a company that has embraced the corporate planning method. Just as it is possible to carry out project planning without corporate planning, it is possible to do operational or strategic planning in isolation. But real success can only come from undertaking both.

Question:

Identify ways of evaluating the evolution of planning thought

Answer:

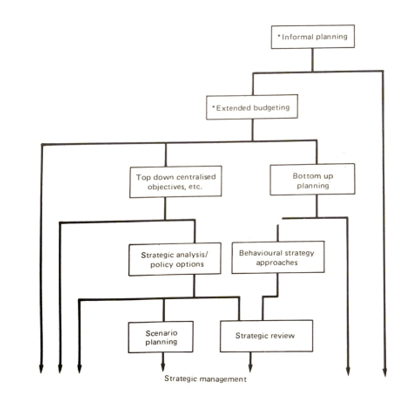

Before we look at ways of moving from the generalized planning system to a continuous management process, it is worth stressing that planning concepts have followed an evolutionary route.

Evolution can be considered in two ways. The first is the way planning has changed within a particular firm. Few people will require more than their own experience to accept the statement that individual companies regularly rethink and redevelop their planning philosophies. For the purist, there is supporting research evidence (see, for example, Formal Planning in U.S. Organisation, H. W. Henry, Long Range Planning, October 1977).

The second way to consider evolution is to define what is generally considered best practice at any time. A real difficulty is that although there is undoubtedly a movement that can be followed, there is never a universal philosophy adopted by all firms. Thus more "primitive" planning exists besides the more advanced forms; as the vocabulary is similar, it takes some time to discover where a firm sits on the evolutionary tree. One way of visualizing this tree is shown in Fig. 2. The arrows indicate that this type of planning continues.

Fig. 2. Evolution of planning approaches.

Another approach to evolution was derived from a research project. This suggested four evolutionary planning phases: basic financial, forecast-based, externally oriented, and strategic management (Strategic Management for Competitive Advantage, F. W. Gluck, S. P. Kaufman and A. S. Walleck, Harvard Business Review, July/August 1980).

Question:

Explain the integration of planning techniques

Answer:

Strategic analysis techniques have improved dramatically over the past decade, and the more modern approaches to planning will make heavy use of some of these. It is a mistake to think of techniques as anything more than a tool kit from which a selection can be to fit a particular situation. Some of the claims made for techniques suggest a solution by looking for a problem, leaving the vague feeling that if the problem does not fit the solution, there is something wrong with the problem!

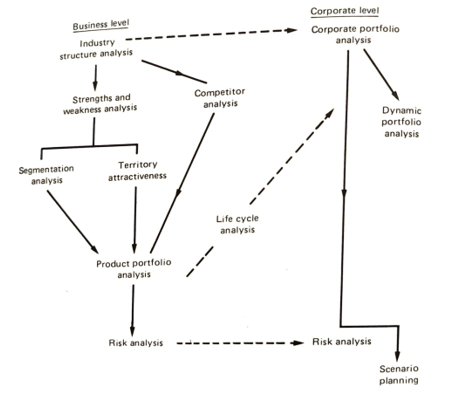

The techniques, many of which are discussed in detail later in this book, need to be looked at as something other than stand-alone features. There is a great deal of value in seeing several techniques as linked, both within a business unit and between the unit and corporate levels, as Fig. 3 suggests. This not only brings recognition that information from one approach can be shaped to feed another, but it also stresses that several should be used to illuminate the problem properly.

Fig. 3. Integration of planning techniques.

In their simplest terms, these techniques change information patterns to perceive the strategic situation differently. All humans erect boundaries of perception when they consider problems because they cannot consider every aspect. Businesses tend to do the same, and a common belief in the strategic situation often permeates the firm. Within this perception, logical decisions are made. In Europe in the Middle Ages, men knew the world was flat and made logical decisions based on this certainty. Once the explorers had proved otherwise, many of these decisions were seen to be illogical. Techniques can fulfil the same function. By changing the perception of the problem, they can show the weaknesses of old strategies and point the way to new ones.

But techniques should become part of the management process. They work when attention is given to the behavioural issues around their usage and good analysis. And this links us to thoughts about the overall shape of the planning process.

Question:

Explain how the total planning process takes place

Answer:

Plans such as those described do not suddenly come into being. One might claim they are in the middle of the planning process. Figure 4 shows the various steps that must be followed before a company can justifiably claim to be formally approaching the task of planning. Each of these steps is vital to the success of planning in the company, and each is described in full detail in later chapters. At this stage, obtaining an impression of the company's total task is only necessary.

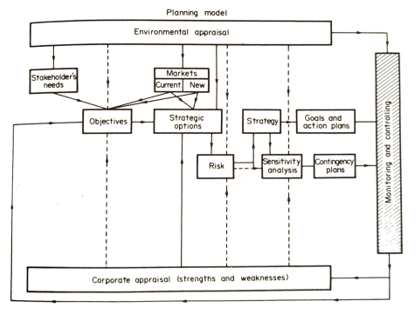

Preceding the diagram is a decision to do the planning. This is a big decision, for it will cause radical changes to the company's management pattern. But it is important to realize that it is a decision. There are several possible starting places for Fig. 4. I have chosen the environment because corporate planning involves acceptance that.

Fig 4. The total planning process

The market has been shown as a separate element from the other environmental factors, affected by them, and vitally important to the company's future. A later chapter deals specifically with market planning.

The environmental appraisal seeks to establish what external events I do affect the company's operations. Equally important, it is designed to provide the company with assessments of future trends to indicate areas likely to change in the years ahead so that that strategy may be adjusted and the company moulded to a new pattern of operations.

As all forecasts of trends are, at best, only forecasts, it will be necessary to reduce these to assumptions for planning purposes (Any plan which provides for future events must be based on assumptions; the corporate-planning process insists that these are clearly defined so that all concerned with planning know what they are) It also makes it possible to monitor them to measure when things go wrong so that corrective action can be taken before the effects are felt on profits.

Monitoring and controlling are seen as a step affecting the whole process, directly impacting the corporate appraisal and the rest of the process. Although illustrated as one step, it will comprise as many sub-systems as needed, and different model elements will be controlled differently. It is a critical stage in the planning process and should be a regular, continuous system.

At the bottom of Fig. 4 is a box indicating the corporate appraisal. This is a very important step but needs to be addressed. Some companies argue that planning should have no connection with present operations: the "don't rock the boat" philosophy. This is nonsense, and unless a company is willing to put itself under a form of self-analysis to assess its strong and weak points, it might as well give up the idea of planning. The corporate appraisal helps the company understand its interface with its environment. It defines, in effect, the unique corporate identity, which is the feature of every company.

Many argue that the true first step in any plan is the definition of objectives. The diagram shows that the primary objectives are, in part, a response to how the chief executive decides to meet his interpretation of the stakeholders' expectations. The stakeholder concept embraces all interests in the firm: shareholders, employees, the community, customers, and suppliers. Although the non-shareholder interests may modify the degree to which profit is sought, we should remember that adequate profit is necessary for the survival and growth of the business and, therefore, to meet the other stakeholders' expectations. The determination of objectives is an area of conflict since everybody cannot be satisfied to the degree that they might wish.

Objectives may require reconsideration during the various stages of the preparation of a plan and are shown in the diagram as being influenced by stakeholders, the environment, the market, the appraisal, and the feedback of results against strategies. The objectives include a profit target, a definition of the company's business, and a statement of what it intends to become. This brief description will be expanded later.

Other stages in the model show the identification of strategic options and considering their risks, leading to a selected strategy subjected to sensitivity analysis to "test" its vulnerability. This is the heart of the analytical framework of the strategic plan and leads to goals and action plans. These effects are the particular operational and strategic sub-plans discussed in Fig. 1.

This leads to monitoring results against the plan and the feedback mechanism already discussed. We are now very close to the design of a planning process. This takes Figs.

The final links which complete the process are forged with other systems in the company: for example, budgeting control, capital budgeting, project and capital expenditure evaluation, personal appraisal, and management development.

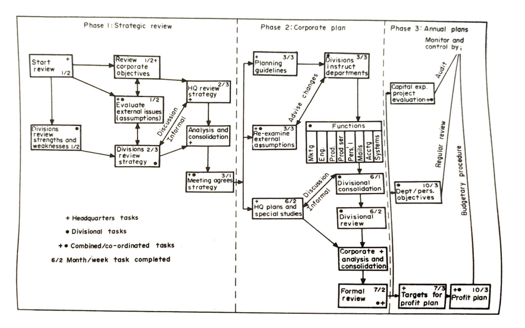

No universal flow chart will illustrate the process in a way that fits every company. The best that can be done is to show a summary diagram of the process as it is applied in a particular company: this is illustrated in Fig. 5. This chapter has dealt at length with some broad issues. Having disposed of these, we can now understand the more practical problems involved in introducing planning and making it work. Figures 1 to 5 should be considered as the various parts unfold over the following chapters.

The emphasis now placed on particular aspects must not lead us to forget the very important relationship each has with the whole.

Fig. 5. Rolls-Royce Motors Ltd. outline planning process. (From Corporate Planning at Rolls-Royce Ltd., R. Young and D. E. Hussey, Long Range Planning. April 1977.)