Get Answers to These 10 Questions Regarding Econometric Demand Forecasting Exam Preparation

What Is Econometric Demand Forecasting, And What Are Its Major Components?

- A priori knowledge of the model;

- Knowledge of probability theory;

- A statistical technique that fits equations to data; and

- Computing power to do the calculations.

| Income | Observed Demand | From A | Squared | From B | Squared |

| 8,000 | 8 | 0 | 0 | 2 | 4 |

| 9,000 | 5 | 4 | 16 | 2 | 4 |

| 10,000 | 9 | 1 | 1 | 1 | 1 |

| 11,000 | 10 | 1 | 1 | 1 | 1 |

| 6 | 18 | 6 | 10 |

What Are The Advantages Of Using The Ordinary Least Squares (OLS)?

The Single-equation Model

Explain Major Assumptions Made Regarding the Listed Models

State Practical Solutions to the Assumptions of the Models

What Are the Limitations of Using the Single-Equation Model?

If we have good-quality data, we may still have the problem. Ideally, we need over 200 observations to operate the best-known aspects of probability theory. If we have fewer data, it is difficult to be confident that our sample represents the 'real' relationship at work. However, it isn't easy to obtain long time series for products. Even when available, their quality is low because the product specification has changed over time. Large numbers of products enter and leave the market every year, and thus our data cannot be long-term. The solution is to simultaneously use cross-section data, i.e. from several markets or customers. This raises the quality problem again.

Shall We Assume The Markets Are Similar, Or Shall We Introduce Another Variable Into the Equation (A Dummy Variable) To Account For, Say, Climate, Or Ethnic Factors?

Some econometricians are now meeting this problem directly by exploring and clarifying the properties of 'small samples', the twenty or thirty observations that are often readily available in many situations.

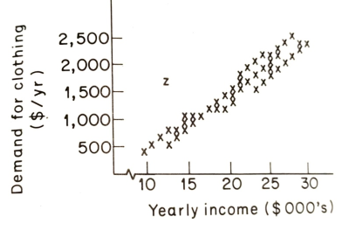

The last problem with data is how to deal with data that are outliers. If we collect data from a questionnaire, we often see a pattern like that in Figure 13.3 with one or more 'outliers' like z.

If we include the observation in our calculations, it will pull the whole line towards it. So, are we justified in excluding it? The answer lies in knowing more about the observation. It may be a mistake, a coded reply, a punching error, etc., which escaped our data-vetting system. If so, it should be disregarded.

Alternatively, it may be genuine but not representative; it may exist but play a larger part in our sample than in the total population. This poses a more difficult problem with three obvious solutions: (i) discard it as over-representing a particular type of consumer or market; (ii) reduce its significance by weighing it by its weight in the population as a whole; and (iii) include it, but mention its biasing effect in footnotes.

The third type of outlier is the hardest to deal with, being both genuine and representative. This is a customer or market which is eccentric. Marketing professionals often solve this problem simply by disregarding it as a special market of its own and thus not relevant to the main study. Cavalier though this seems to some 'scientific' observers, it serves to produce more easily communicable results. Moreover, the extra variable needed to 'explain' the behaviour of the eccentric consumer may not be worth its cost. Forecasting is, after all, an economic activity - the marginal cost must be less than the marginal revenue!

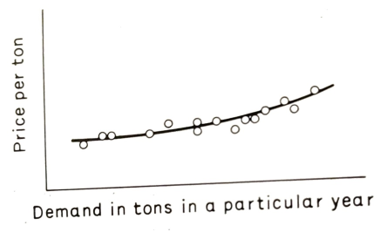

The identification problem, one of the classic early statistical studies of demand (Working, 1927), used time series for the price and demand for pig iron in the late nineteenth century. The result was a curve like that in Figure 13.4.

Establish the Identification Problem for the Demand and Supply Curves

One of the classic early statistical studies of demand (Working, 1927) used time series for the price and demand for pig iron in the late nineteenth century. The result was a curve rather like that in Figure 13.4.

This might lead us to the conclusion that demand rose when the price rose, the opposite of the usual relationship. However, the obvious question is whether we have a demand curve before us. In demand and supply analysis, actual prices are where demand and supply curves cross, so any one of the observations would be on both the demand and supply curves for that year. We would only trace the demand curve if it did not shift and the supply curve did.

Fig 13.4 Demand curve for pig-iron

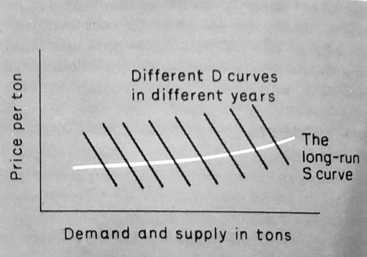

What is far more likely is that the supply curve for pig-iron shifted a little over the years, but demand was affected by the rising output of steel, railways, ships, etc. Figure 13.5 illustrates this.

This historical digression is included because one of our main problems in analyzing data is identifying the relationship that we have calculated or plotted. To plot the demand curve for a product, we need to find a variable (shift variable) that will shift the supply curve. Again, going back to the introductory economics, technology will shift demand curves. Remarkably, there is a connection between the simple graphical analysis above and the complications needed to analyze some markets that cannot be tackled using single equation methods. In both cases, it is the existence of shift variables that solves the problem of identification.

What Is The Basis Of The Specification Problem Established In The Equation?

The specification problem lies in knowing whether the right variables have been included on the forecasting equation's right-hand side (RHS). We can summarize the problem by saying there must be enough variables and not too many. First, how can we ensure that there are enough? As usual, the answer lies in combining economic and statistical knowledge. Suppose we use methods to analyze some price and demand data and find that it shows a positive relationship. In that case, our economic knowledge tells us that D = a + bP is insufficient to explain what has happened.

Fig. 13.5 Long-run supply curve for pig-iron

If demand rose while the price rose, another variable is likely to have caused it. Thus we change our model to D= a + bP + CY assuming that income (Y) has increased and demand to increased despite the price increase.

Give an Example Explaining the Effects of These Variables

Deciding when we have too many variables in the RHS is a little more difficult. For instance, we assumed that car ownership was based on price, income, and educational level. We might easily put data for different countries into a regression program and find results like D = 0.1 x Population-0.2× Price +0.013 x Y + 0.06 x years of education. This looks interesting until we realize that there is a very close relationship between income and education. We speak of these two variables as being mutually correlated or collinear. They break one of the initial rules of the linear regression model that the RHS variables should be independent. If collinearity exists, the parameters (calculated by the regression program) will be meaningless, and the usual solution is to discard all except one of such variables. This is another reason why many forecasting equations feature income: it is strongly correlated with so many variables that it often supersedes more obvious variables in forecasting models.

When Does The Problem Of Simultaneity Occur?

When one of the RHS variables is affected by the 'dependent' variable, then we have the problem of simultaneity. For example, if we have the equation = an x bp + cy but know that the price will differ when demand changes, then we have a problem. We need to know the relationship between price and demand; in other words, we need at least one other simultaneous equation to describe the market in question. For example, in functional form:

D= f1 (P, Y)

S= f2(Y)

P = f3(S, D)

Y = some value

There are three solutions to the problem of simultaneity. First, we can select only problems where single equation approaches will work, i.e. where all the RHS variables are genuinely independent. Allan discusses a possible example in further reading. The second approach is to collapse all the simultaneous equations into one 'reduced form' equation, ensuring that all the RHS variables are genuinely independent. The third approach uses more complex estimation techniques than ordinary least squares.

Technique bias

Any estimation technique c can be assessed for bias, consistency, and efficiency. It is said to be efficient if it gets results closer to the 'true' parameters than other techniques. It is consistent if the larger the sample, the nearer to the 'true' parameters it gets. Finally, it is said to be unbiased if it gives the 'true' value of the parameters as opposed to consistently or underestimating them. OLS is biased if the data do not conform perfectly to the linear over or regression model assumed (i.e. dependent variable forecast by independent variables). Thus it produces nonsense results in situations such as the pig-iron one we mentioned above or any situation where its assumptions are violated.

Thus we have the overwhelming problem of an estimator who is biased in almost all the cases we are likely to find in forecasting, and managerial economists have tackled this in three ways:

- ignoring the problem, which is inexcusable.

- finding cases where it is accurate enough.

- using in- increasingly sophisticated econometric methods.

Perhaps the most encouraging way to end this chapter is to reiterate my belief in mixtures of techniques for solving problems. Econometrics is not the answer to forecasting, but it is a very useful addition to the forecaster's toolkit.