Guidance for online Inflation and Unemployment Midterm Exams

Why were the economic policies formulated in the 70s dominated by the problem of inflation?

Explain how the Philips curve is used to explain the dynamic behavior of a macro model

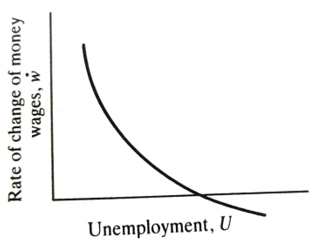

Figure 7.1 The Philips curve

Discuss the major disagreement in the causes of inflation in relation to aggregate demand and supply

The major disagreement over the causes of inflation is often characterized as being between those who think it comes from aggregate demand and those who think it comes from the supply side of the economy. Most would agree that an expansion of the money stock is necessary to sustain a price-level rise, but those who believe in cost-push usually argue that the money stock has to be expanded in the wake of inflation to avoid unemployment. Both lines of argument could be valid. The question & what actually happened in any particular episode? Let us first look at the price level and the level of output in terms of Model III. Following Gordon (1978) it is convenient to combine the two versions

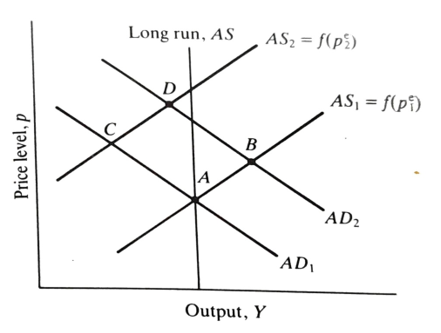

Model III a simple modification of the aggregate supply curve. For the short-run case where money illusion was assumed on the part of suppliers of labor, we assume that labor supply depends upon the expected price level Demand for labor on the other hand depends upon the actual price level. In the short run, while expectations lag behind reality, the aggregate supply curve will be upward sloping but it will shift leftward if expectations are revised upwards. In long run expectations are correct so the long-run supply curve is vertical at the trend output level sometimes called the natural" output level. In other words, the long-run supply curve shifts rightwards each period because of the underlying growth of the economy. If we consider the initial position in Figure 7.2 to be at point A then it is dear that a price-level rise can be started by either a rightward shift of aggregate demand AD,, or a leftward shift of aggregate supply. A cost-induced inflation would involve a supply-side shift and the economy would move from A to C. A move to D would then follow if measures were taken to eliminate unemployment. Eventually the system would settle again at a higher price level on the long-run aggregate supply curve. A demand-induced inflation, however, would be caused by a shift of the demand curve to, say, AD, so the economy would move from A to B. Expectations would then be revised so that AS, would shift in the direction of AS, and the economy would move to a point like D. Whether D is in this case to the left or right of long-run AS does not matter- either is possible. The point is that a demand-induced inflation will move the economy through an anti-clock wise arc initially. A supply-induced inflation will move it through a clockwise arc.

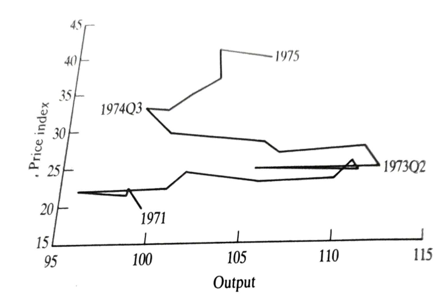

The picture in the United Kingdom in the early 1970s is extremely clear, as Figure 7.3 shows, so long as it is appropriate to start the cycle in 1971. The end of 1971 marks the beginning of a major expansion of the money supply associated with Competition and Credit Control, and March 1972 was the date of Mr Barber's famous expansionary budget. Hence a shift of demand moves the economy along a short-run supply curve, which incidentally appears to be fairly flat. After the oil shock (and a further supply-side squeeze following from a spectacularly badly timed attempt to introduce indexed wage contracts just when retail prices were unexpectedly rising steeply) there is a dramatic leftward bounce in output to the trough in late 1974. While the adverse supply shift does not go away, the effects of the Barber boom persist and the economy slides up the short-run supply curve as demand recovers.

Notice that while the movement from 1973 to 1975 must involve a shift of the supply curve, some such shift would be an essential part of the demand- induced story. The economy cannot stay at a point like B in Figure 72 because it is beyond the long-run supply curve. Price expectations will necessarily shift the supply curve leftward sooner or later. It is quite likely that the oil price rise induced the shift of supply between 1973 and 1975, but it is important to realize that after the events of 1971-73 some such shift would have occurred anyway due to the behavior of expectations.

Figure 7.2 Aggregate supply and demand with price expectations

Discuss using a diagram the expectations of the augmented Philips curve

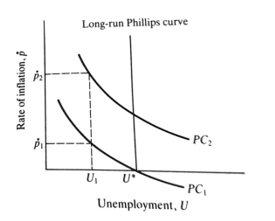

An analogous argument can be developed in the more familiar dimensions of inflation and unemployment. It was seen above that a single stable Phillips curve is incapable of reconciling the observation of both high inflation and high unemployment. However, once it is admitted that there is a new higher Phillips curve for each higher expected rate of inflation events become easy to explain.

To see this, suppose curve PC, in Figure 7.4 is the Phillips curve for zero expected inflation. If the level of unemployment is U, this expectation will be fulfilled and nothing needs to change. However, if unemployment were U inflation would be greater than zero at p. In effect, the wage bargainers made a mistake setting wages inflation turned out to be higher than they expected (the expectation error is positive). Friedman, using a form of adaptive expectations, argued that having underestimated inflation, the nest period expectations would be revised upwards. This generates a higher Phillips curve, says PC, Again, inflation would be higher than expected and, so long as unemployment stayed at U, inflation would accelerate. So long as we remain to the left of U. inflation carries on increasing consequently, we call this the 'accelerations' hypothesis. We can think of the long run as the period within which expectations are fulfilled. As a result, the long-run Phillips curve traces out the point on each short-run curve where expectations will be fulfilled and where inflation is consequently stable. The dramatic conclusion is that the long-run Phillips curve is vertical by definition. There can be no long-run trade-off between inflation and unemployment.

Friedman referred to the unique level of unemployment at which expectations turn out to be correct as the Natural Rate of Unemployment, also known as the equilibrium rate. He made very large claims for this rate, which we now know to be unjustified:

The natural rate of unemployment is the level that would be ground out by the Walrasian system of general equilibrium equations, provided there is embedded in them the actual structural characteristics of the labor and commodity markets, including market imperfections, stochastic variability in demands and supplies, the cost of gathering information about job vacancies and labor availabilities, the cost of mobility, and so on. (Friedman, 1968, p. 8)

'Natural' carries with it the implicit connotation that it is also 'best' but the equilibrium rate, even in the absence of powerful unions, will generally be inefficient. This is not the place to rehearse the arguments, but it turns out that the natural rate may be too high or too low, as the factors pushing is away from efficiency can go either way; see Pissarides (1990) for an exhaustive discussion of the issues. Thus a preferable, less value-laden, term for the unique long-run level is the NAIRU, or Non-Accelerating Inflation Rate of Unemployment. However, the term 'Natural Rate' is still a useful one to keep. As we see below, the concept of the NAIRU can be fitted into the wage bargaining model set out in Chapter 5, and it is useful to think of the natural rate as the level of unemployment that would prevail in the absence of any union bargaining power. It is important to bear in mind that it is unlikely to remain constant over time. For instance, if unemployment benefits fell it is likely the unemployed would want to spend less time searching for work, and the natural rate would fall. This will affect the NAIRU. However, as we will see, other factors (such as trade union legislation) can also affect the NAIRU, even if the natural rate is constant.

Figure 7.4 Shifting Philips Curve

Using Friedman’s version of the Philips curve, explain how the Philips curve shifts in a unionized economy like the United Kingdom

Friedman had in mind a competitive world where atomistic firms compete and individual workers search for work. What drove his version of the Phillips curve were unemployed workers mistakenly accepting high money wage offers, wrongly thinking that they were high real wages. In order to understand how the Phillips curve shifts in a unionized economy like the United Kingdom, we have to consider the bargain struck between firms and workers.

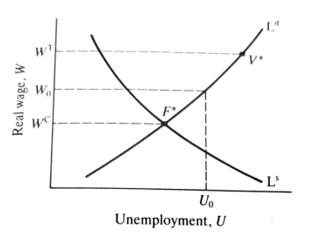

The issue of firm/union bargaining was addressed, and this section builds on that analysis. As argued in that chapter, firms and unions both have ideal targets for the real wage. The firm would like wages to be set at the minimum market rate. This sets a floor; if the wage were any lower, the firm would be unable to employ enough workers. Ceteris paribus, unions want a higher wage, but as they recognize that higher wages imply lower employment, their ideal wage takes into account the consequences for jobs, balancing higher wages with laid-off union members. We assume that firms have the 'right to manage', so we are always on the demand curve. While this is technically inefficient, as discussed in Chapter 5, the evidence is that it is the realistic assumption. This leads to Figure 7.5.

The figure assumes there is only one (representative) firm so we can work directly with unemployment. Thus L is the conventional labor demand curve, which slopes upwards when unemployment (rather than employment) is on the horizontal axis as drawn here, and L' is labor supply. Vis the union's ideal point, with associated real wage WT; F is the firm's ideal at the competitive wage W. The actual outcome is at Wo and Uo. The determinants of Wo (and therefore U) are the factors that affect the target wage, the competitive wage, and the union's relative bargaining power. The competitive wage can be thought of as being determined by the natural rate of unemployment; if this increases, effective labor supply falls and the competitive wage rises. So anything that affects the natural rate affects the competitive wage. Factors likely to increase the natural rate are the degree of mismatch or 'noise' in the labor market, like the disparity between the type of jobs available and the skills of those unemployed; the level of unemployment benefits, which affects the length of time the unemployed spend hunting for a job; and institutional factors like the social stigma attached to unemployment, or the administrative structure of the government employment services.

The union wage will similarly be affected by several factors. These include union preferences; if unions become more 'militant' it may be reflected in a push for higher wages. Other factors include the level of unemployment benefits or wages in any non-union sectors, which soften the impact of job losses on union members, and the level of aggregate unemployment itself. The higher is unemployment, the more serious is the effect of a lost job, as laid-off workers tend to spend longer between jobs.

The actual outcome will depend on the relative bargaining strength of the two parties. This will be affected by legislation, and also by the ability of one party to impose costs on the other. For example, a high level of capita intensity makes it easy for workers to impose large costs on employers i the event of a strike, as although there are no wage costs during a strike capital and other fixed costs are still incurred. Strikes might also be more effective when demand for the product is buoyant, as lost profits a Finally, note that a contraction in demand (a rightward shift in Lin Figure 7.5) will tend to lower the bargained real wage, as the competitive wage is lower and higher unemployment for any given wage will tend to lead to a downward shift in the union target wage. Putting these factors together, the wage bargain is given by: are high

W = Pf(u,z) (7.1)

The nominal bargained wage, W, is proportional to the price level, P. negatively related to the unemployment rate u, and affected by other factors, z, including the level of unemployment benefits and aggregate demand. However, we need to recognize that firms and unions must form expectations of the price level. We begin, where lower case letters indicate logs, by rewriting (7.1) as

w = p² + g(u,z) (7.2)

The log of the wage, w, is equal to the log of the expected price, p. and negatively related to the unemployment rate and other factors, Next, note that the actual price differs from the expected price by an error term, &:

P = p² + ε (7.3)

The log of the actual price, is equal to the expected price, p. plus the expectation error, &. Next, we need a story about what determines prices. It is natural to assume that prices are a mark-up over wages, so

p = w + h(z) (7.4)

The price level is a mark-up over wages. The mark-up, h, is affected by a range of factors including aggregate demand. We have again used a log-linear form to simplify the equation here, and abstract from other costs (such as energy, import prices and taxes) although in practice these are potentially very important. Putting prices, wages and expectations together, we get

p = p + j(u,z) (7.5)

Where j(u,z) conflates g(u,z) and h(z). Equation (7.5) is about the price level not inflation, but we can easily transform it into a Phillips curve. Recalling that P, PP-1 and p, p,-P-1 (as P-1 is known at time t), subtracting p,-, from both sides of (7.5) yields

p = p² + (uz) (7.6)

This tells us that for given z there is a unique level of unemployment at which expectations are correct where p = p-defined by the value of u that satisfies

0=j(u,z) (7.7)

given z. This is the NAIRU, and varies as z changes. Later in the chapter we look at what actually happened to z and the NAIRU in the 1970s and 1980s.

Figure 7.5 The wage bargain