6 Key Questions and Answers to Help You Learn How to Tackle Exam Questions on Pricing Problems Correctly

With the help of a graph, explain and illustrate the effect of monopoly on resource allocation.

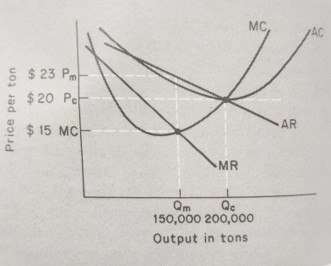

Fig.6.2 Effect of monopoly on resource allocation

The effect of making an industry a monopoly, whether owned by the state (as in the UK) or regulated by it (as in the US), would be to reduce output and raise the price if the monopoly were allowed to 'exploit' its control of the market, a position illustrated in Figure 6.2.

The assumption is that the diagrams refer to a single plant, say a small coal mine, which is originally a price-taker, and then, with the formation of the monopoly, becomes a price-maker. The AR (demand) curve must face the same output and price as before, but it is now sloping; thus the management can now choose, for the mines as a whole, to raise the price. This results in lower output QM rather than QC, and higher price, Pm rather than Pc, and the customers are being charged more than the marginal cost of supplying them, and thus will consume less of the product than its resource cost would justify.

What are some of the problems associated with resource allocation and marginal cost pricing in an economy?

We can divide the problems into those which concern the particular industry and its customers and those which impinge on other industries and customers.

The first problem concerning the particular pro- duct lies in identifying what marginal cost is. In the short run, it is clear which resources are used up in producing extra output, for example, extra fuel needed by a plane to carry extra passengers or by a power station to produce extra electricity. Thus short-run marginal cost can be calculated fairly easily. However the plane or power station has to be replaced in the long run, and thus the total costs of production must be found by someone. Deciding which of these long-run marginal costs should be allocated to which customer was difficult - should they be allocated equally, or based on the level of demand? If the latter was done the result was to have charges which could no longer be called marginal cost-based.

The next problem was the cost of finding out the marginal cost, if it was different for different customers, and charging each one an appropriate amount. We can see this problem clearly if we take the examples of bus travel, electricity, and water. In the UK it is usual to charge for bus travel by the distance traveled. This necessitates someone to calculate and collect the fares, and in some cases, the cost of collection exceeds the fare! One solution is for the driver to collect fares but this slows down the service, imposing a cost (in time) on the passengers and other road users. A common solution in the US is to charge a flat fare for a day's bus riding, say $1, thus cutting out fare calculation and loss of time by the driver and passengers. Similarly, electricity meters are a way of charging customers which is simpler and cheaper if they charge per unit consumed. Meters are now in use in the UK which charge night-time electricity at lower rates, but their higher cost reduces some of the benefits from reflecting the lower cost of night-time generation in prices. The cost of producing electricity fluctuates throughout the day and year, and the more sophisticated meters which would reflect this are now almost justified by the rising cost of energy. Water is another product where metered supplies for domestic consumers may be cost-effective if water costs go up much more in the UK. (Currently, the payment for water is based on a property tax basis, as with other state services provided locally.)

The third problem often called the peak problem is caused by short peaks in demand for public utilities which cannot store their product. Thus we have an electricity-generating plant which is only needed for the morning and evening 'peaks", and buses and trains which are similarly under-utilized for most of the day. From the resource cost point of view, it is clear that the peak customers should be charged for the facilities which they alone use, so charges should be higher at peak times. This raises two related problems, the equity of charging more and customer resistance to it. Rush-hour travelers often complain of crowded conditions and regard higher fares as adding insult to injury. Furthermore, many of them can only be induced to travel on public transport by making the fares attractive.

The last problem within the product market itself is how to finance the replacement of equipment. If the customers have been charged the short-run marginal cost they will not have paid the total cost, and would not do so in the future either. This can be seen very clearly with transport facilities in most cities-roads, bridges, tunnels, and rail facilities are not fully paid for by their users. Periodically this causes crises when the government has to decide whether to build a new road, airport, or channel tunnel or provide funds for electrifying a rail line or replacing commuter rail vehicles. If the customers had paid the full cost or could be expected to do so in the future, there would be much less of a problem and perhaps less public agonizing over whether the investment should be undertaken.

What are the general rules for resource-efficient pricing by public utilities?

Bearing in mind the problems just outlined, can we produce any general rules for resource-efficient pricing by public utilities? The topic is an enormous one, but we can suggest four useful points which have come out of work by economists on the topic.

The first is that public utilities should try to approximate their charges to long-run marginal cost to provide for both efficient resource allocation and replacement of capital equipment. This will mean that demand is not unduly stimulated by charging only short-run marginal costs, nor stunted by charging as much as the traffic will bear, thus maximizing profits. Thus weak customers with no alternative should not be exploited, merely made to pay what it costs to supply them.

The second point is that, as French electricity economists have shown (Boiteux, 1965), long-run and short-run marginal costs are the same when the utility is running at its designed output. Thus short-run pricing can be used to expand demand to capacity, and the short-run price will gradually approach the long-run price as capacity is reached.

The third point is that we should not worry too much about pricing exactly at marginal cost in an imperfect world. There are many industries where price does not equal marginal cost, perhaps as a result of elements of monopoly. This point has often been made rather despairingly, implying that the existence of monopolies elsewhere means that the marginal cost rule must be discarded. What the studies show is that unless the other industries have their prices widely different from long-run marginal cost then the pricing of the public utilities does not have to vary very much from the theoretical rule to compensate for imperfections elsewhere. Thus small deviations from marginal cost are not very significant.

Lastly, the customers who suffer by paying the 'true' cost of the services they receive can always be compensated by 'transfer payments' from the state, and most economists agree that this is more effective than giving them services below cost. Thus in the UK the old and disabled are given financial assistance to use transport, and in the US the poor are given food stamps, rather than charging them lower prices for one particular product.

What are the three distinct stages in the evolution of policy for the state-owned industries in the UK?

Most (coal, electricity, gas, railways, airlines) were nationalized between 1945 and 1950, and at that time were merely instructed to 'break even' after paying interest on the public money invested in them. In economic terms it was equivalent to telling them to make 'normal profit', assuming that the owners - that is to say, the citizens - were satisfied with the interest rate. In pricing, they were left largely to formulate their policies, and the railways and coal industry adopted uniform prices per passenger mile and ton of coal of a particular type irrespective of the cost of production. This 'average cost pricing' led to cross-subsidization in both industries. The customer supplied with high-cost coal, for instance, paid the same as those supplied with low-cost coal. Thus 'uneconomic facilities' were kept in production, and some customers received well below cost. The effect of these policies has been disputed, but we can say that they probably cushioned many workers and customers against changes that would otherwise have been more painful, but reduced the competitive strength of both industries. This be- comes more obvious when we contrast the electricity and gas industries where prices were largely marginal cost-based. Electricity demand was ex-pending, but gas like coal and railways was a declining industry. Gas, however, was able to invest rationally because of its cost-related approach, and thus move from manufactured gas to natural gas as it became available, and then expand again.

In the 1960s the government formally instructed the industries to price according to long-run marginal cost and gave each of them different targets according to market conditions. Thus the airlines, gas, and electricity were to make returns over the cost of interest, but coal and railways were allowed to make less. There was to be an approach to running the industries based closely on economic principles.

The third stage started with the publication of the 1978 White Paper (policy statement) on the nationalized industries. The main change envisaged was the conclusion of the RRR or required rate of return into any calculations on investment or pricing. This was partly just an increase of emphasis, because each industry had been given targets for returns since the 1960s, and thus implicitly was expected to take them into account in investment and pricing. However, it also reflected the Treasury's move towards 'accounting' as opposed to 'Economic' controls. The 1970s had seen the imposition of 'cash limits' on public spending programs when the previous type of budgeting in real terms' had produced runaway spending during fast inflation Thus the industries were not only to have their spending controlled in cash terms but also to have financial targets explicitly included in investment and pricing decisions. This does not mean that prices would not reflect marginal costs, it is just price-setting a little more complicated as Baumol and Bradford (1970) have shown.

Thus, in general, the pricing of UK nationalized industries is related to long-run marginal costs However the actual prices charged have been subject to considerable 'external shocks' of three kinds. The fuel industries have been shaken up by the oil price increases of the 1970s which enabled the coal industry to absorb huge wage increases, and still, retain its share of the energy market Electricity suffered vis-a-vis gas because its costs went up while natural gas contracts kept gas prices from rising as fast. The next, smaller shock has been felt in the passenger transport business as a result of the increasing emphasis on passenger subsidies from local government (political) decisions rather than other travelers. Thus local decisions in one area of the country can change the prices which travelers have to pay for bus or rail transport.

The third shock to prices has been the inability of governments to refrain from interfering in pricing. Thus we have seen Labour governments preventing price increases to encourage people to accept lower wage increases, and Conservative governments insisting on price increases to reduce the PSBR (public sector borrowing requirement).

Briefly describe the six distinct strands in the regulation of public utilities in the US

- The distrust of monopoly power, and thus the regulation by the Federal government of products in inter-state commerce such as oil products and natural gas, and by the state governments of public utilities such as bus, natural gas, and electricity services. Many states have public utility commissions whose primary duty is seen as protecting the consumer from the. power of 'natural monopolies'

- The strong commitment in public discussion to marginal-cost related prices, and thus lower rates for large customers, and those consuming when costs are low.

- The move in the late seventies to 'de-regulate" several industries at the Federal level to encourage 'conservation by price' for such products as gasoline and natural gas. Similarly, the gradual de-regulation of internal air services and inter-state trucking is expected to improve resource allocation. In both cases, there is some provision for subsidies or transfer payments to help those hit by higher prices or withdrawal of services.

- Another recent tendency is to use public utilities for social and political objectives. Thus the utilities are made to provide small amounts of gas and electricity at 'lifeline' (cheap) rates, and even encouraged to lend customers money to insulate their houses.

- The fifth phenomenon which we can observe in the US may help to account for some of the above conflicting moves. There is a general insistence amongst both economists and politicians that regulation must be seen to produce results at least equal to the cost of regulation. Thus different approaches are justified in different cases.

- Lastly, we have a paradoxical result of regulation, in some industries, an apparatus set up to protect customers has become an apparatus to protect producers. Rates of return are controlled, and while this might, at first, have kept down prices, it may now be working to keep them up. The regulatory body may have been effectively captured by the industry it was set up to regulate. For instance, part of the cost of nuclear power stations not being used is being met by the customers in higher tariffs, rather than being completely borne by the shareholders. Thus the idea of a 'fair return' means that investment mistakes are not penalized as much as perhaps they ought to be.

In summary, the US regulation of public utilities does appear to have many economic principles in common with the UK policy for nationalized industries.

Discuss in detail the concept of transfer pricing in private firms.

Private firms have a resource allocation problem when they trade products within the firm. The prices used, often called transfer prices, have to be consistent with the firm's objectives. If the firm is a profit-maximizer it should contribute to this end, rather than waste resources. We can simplify the problem to a choice between two alternative approaches.

One alternative is to treat the different parts of the firm as if they were independent of each other, selling at prices that cover the cost and make a normal profit. Some firms do operate in this way, although it is often arbitrary which of their goods are 'sold', and which are merely 'supplied' to another department. Thus some car manufacturers insist that their component divisions compete with outside suppliers and that this provides a stimulus to efficiency. The freedom to set prices does not of course guarantee that they will be related to resource costs, which will depend on the market conditions.

The other alternative is to treat the firm as if it were a 'planned economy' with goods being transferred between departments by order from above and at prices reflecting the 'costs' involved. How these costs are calculated is covered in management accounting texts but we can state the general principle here. The firm will be best served when the internal prices reflect the marginal costs of the goods traded. Supporting a loss-making division from the rest of the firm can prolong its life, but also destroy the morale and sales of other departments. The more vertically integrated the firm is, the more it faces this problem. The temptation is to price the component at short-run marginal cost to appear efficient, but this only puts off the day of reckoning, for sooner or later the capital plant needs replacing, and then it is obvious that there is no way of covering the long-run marginal cost. Thus underpricing car components produce much the same results as underpricing commuter rail travel, a crisis when the capital plant has to be renewed.

In summary, marginal costs provide valuable guidelines to transfer pricing by firms.