Spring 2022 Semester Exam Solution on Incorporating Externalities Into Decision Models at Princeton University

how does incorporating externalities into decision models benefit the government and its subjects?

Many decisions affect those not taking the decision. If the decision-taker pays the effect or can be included in the price of the product, it will be considered when making the decision. The effects not considered are called 'externalities' by economists, and the chapter starts by defining them. It then shows how externalities are dealt with in the public and private sectors. The government can analyze externalities using cost-benefit analysis, and we look at how such analysis might be conducted. With private sector externalities, we look at how both the government and firms can deal with them.

Externalities

We can analyze the effect of any decision by dividing the results into costs and benefits. Some of the costs will be borne by the people taking the decision and passed on to the customer. Similarly, some benefits will be such that someone can be charged for them. These are called internal costs and benefits. The total cost and benefit balance will only be found when the external costs and benefits are considered. In an equation:

Internal cost +external cost social (total) cost internal benefit + external benefit social (total) benefit

Thus a private sector decision-taker would normally consider the balance of internal costs and benefits, what he would have to pay and what he could charge someone for. If the externalities had a different balance, his decision would not reflect the wishes of society as a whole. A commercial TV network might discontinue 'educational' programs because the advertising attracted was not sufficient to pay for the programs. Viewers might feel differently but not be able to influence the network. The internal balance is negative, but the social balance is positive. In another case building an oil refinery might be cheapest at a particular location next to a housing area. The internal balance is positive, but the social balance might be negative when the unpleasant smell is considered. This short account of external ties raises two related questions: how can we measure externalities, and what decision-taking technique can best deal with them? The rest of this chapter answers the questions, first for the public sector and then for the private sector.

Cost-benefit Analysis

The public sector has dealt with the problem of measurement and decision-making on externalities in two major ways. The first is the use of the political process. People affected adversely by a government or nationalized industry decision act can be compensated or reversed. People who would benefit from a project are put under political pressure for it to be carried out. Most countries have many examples, and presumably, the strength of the political pressure is a measure of the external cost or benefit.

Political scientists and economists disagree about the value and accuracy of the political process in reflecting the size of external costs and benefits. Part of the dispute is about how the political process in different countries/regions operates, but it is also about how we can quantify human feelings. Political scientists see the political system as a sophisticated way of expressing people's choices. Economists see market forces as measuring those choices more accurately. Before making any judgment, we should look at how economists propose measuring externalities and making decisions involving them. (The further reading contains the views of one of the strongest opponents of the economists' approach.)

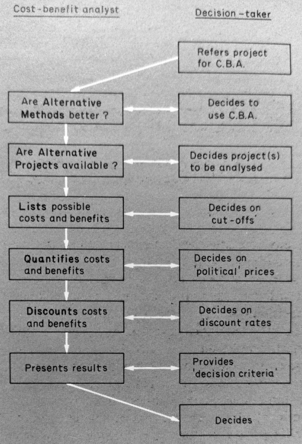

The economists' approach is often given the collective label of cost-benefit analysis, or in the US, benefit-cost! Looking at a complete, idealized analysis of a project should make the theory and method clear. It is outlined in Figure 19.1.

Fig. 19.1 Cost-benefit analysis: flowchart

We immediately notice two aspects, the strict division of responsibility between the cost-benefit analyst and the decision-maker and the continual interaction between them. Many of the cost-benefit studies which have aroused public (and professional) controversy have neglected either or both of these 'ideal' aspects. If the analyst is seen to have been taking decisions unconsciously, and if the true decision-taker has not been fully involved, then the study will not be consistent with other decisions and is likely to be repudiated when opposition appears. As we go through each activity stage, examples of the problems will be seen.

Alternative Methods?

It may seem curious that one of the first questions a good cost-benefit analyst should ask is whether other analysis techniques would be more appropriate. However, CBA is expensive and time-consuming, and in its youth in the 1960s was often suggested because it was new rather than because there were significant externalities to consider! For example, when governments were considering projects, they specified CBA studies when they wanted to know only the effects on their revenue and expenditure. For this, an ordinary investment appraisal would have been sufficient as they were not interested in effects on others or non-monetary effects. Similarly, there are projects for which the objective is clear, and there are not likely to be different benefits from different methods. For example, raising literacy levels, delivering nuclear weapons to a particular country, and producing more business graduates all have a stated objective that can be achieved in several ways. Thus the correct analysis would appear to be finding the cheapest method of achieving the objective, sometimes called a cost-effectiveness study, a method that is much cheaper than CBA.

Alternative projects?

One of the characteristic contributions of economists is to suggest overlooked alternatives. For example, a water-supply project may be 'needed' because people do not pay the true cost of the water they consume. So an alternative project would be installing meters and charging the true cost or simply asking people to conserve water, which has worked in some cases. Only the decision-taker can decide whether the alternatives are politically feasible. Still, the economist can point out that the relative costs may influence the electorate's political judgment. Outstanding recent examples of the value of alternative strategies in the UK have been the expansion of the capacity of London Heathrow through the use of wide-body jets, which has postponed the need for a third London airport, the use of very high subsidies to firms to locate in areas of high unemployment as an alternative to social security payments and law and order costs, and the switch to subsidies to renovate housing as opposed to heavy subsidies on new local authority housing. In none of the cases were CBA studies undertaken, but the advice of economists was pressed on the relevant decision-takers through the political process.

Listing costs and benefits

When the study at last starts, the first activity is to list as many effects of the project as possible. Three questions arise at this stage: distributional changes, diversionary effects and the choice of cut-off points

By distributional changes, we mean the project's effect is benefiting some people and harming others. If we are content to assume that $1 taken from someone is worth the same as $1 given to else, then we are said to be ignoring distributional effects. If we do not value the equally, we have to decide how to compare different people's losses and gains or to list exactly how the project affects different groups. The latter is often the easiest course of action and fits best with economists' usual preference for showing the decision-taker as much detail as possible. The more detail shown, the more likely it is to be the decision of the decision-maker rather than the analyst. Analysts may have preferences for worthy groups in society, but if the gainers and losers are made public, it can be left to the political process to decide. As economists, we cannot criticize the political process as a means of taking decisions, but we can insist that all the relevant information should be known. Thus, CBA has at least a minimal role in searching out some of the projects' distributional (income transferring) effects.

The next problem at the 'listing effects' stage is whether to record the diversion of costs or benefits; an example of this might be a new road that transfers trade from one garage to another or an airport plan which inflicts noise on one group of people rather than another. If the amount involved is equal, should we bother about it? The answer depends on our previous question. If we are interested in distributional questions, we must list all diversions of costs or benefits. If we are not, we must not list any of them and only consider net changes in costs and benefits. The third problem faced when listing costs and benefits are perhaps the easiest to solve when to stop listing! For example, a project in the UK will affect the Republic of Ireland and France, but the UK decision-taker may say we should not bother them. Similarly, there may be effects judged too small to be worth computing, such as savings in time of fewer than five minutes on a journey or savings in the cost of less than 5% of the total cost of a journey, so these become the cut-off points.

With each of these decisions, the clear distinction between the analyst and the decision-maker enabled the decisions to be taken openly and recorded clearly in the final report.

Quantifying costs and benefits

When quantifying costs and benefits, we are in a complex and controversial area. However, we can identify some general principles, which we can term market prices, shadow prices, standard values and political prices. Each value is appropriate in particular circumstances; between them, they cover many 'problem areas".

Market prices will be used to value costs and benefits when they are available. This is based on one of the central tenets of market economics, that prices represent what people are willing to pay and what they are 'willing to supply. Thus actual prices represent the valuation by the participants in a particular transaction. The participants may be unequal in their economic power, which may be personally distasteful, but some things are outside the scope of our project. Monopolies of buying or selling goods and services distort prices, but their effect should be noted rather than attempting to make calculations as if they did not exist.

Shadow prices can often be calculated where something is never directly sold. For instance, we can estimate the value people put on their leisure time by seeing on what terms they are willing to give it up. i.e., work extra hours voluntarily. We can put a value on their leisure time related to the rate of pay they are willing to give it up. Similarly, we can make assumptions about the value people place on a relatively quiet housing area by looking at how much fewer houses in noisy areas sell for or how much people voluntarily spend on noise-proofing. In each of these cases, we are following similar logic to the market price example, looking at how the participants appear to value the costs and benefits that occur.

Sometimes, the decision-taker already has sets of shadow prices used in its CBA studies, often called standard values. For example, the Ministry of Transport in the UK applied a consistent set of values for 'passenger time saved' to CBA studies done for it in the late 1960s. Using these values ensures that the CBA studies will be consistent with each other and with other decisions using other techniques. Again we are looking at how the participant in a decision, in this case, a government department, values a cost or benefit, and we use this value. An obvious advantage of standard values is that they can be improved by public debate amongst economists.

If none of the previous sources of values is used, then we are left with some costs and benefits without money values on them. One alternative is to list them as an appendix to the final report: the other is to value at least some of them using political prices. The case of Stewkley Church in the Third London Airport CBA study neatly illustrates the process of finding political prices. The eleventh-century church would have had to have been demolished to make way for one of the airport sites. It was originally given a shadow price equal to its insured value, the reasoning being that this must be what it was worth to its owners! Objectors to the particular site claimed the church was unique and thus priceless. Both valuations were in error: the fire insurance value was too low, but the value was not infinite. Thus someone should have taken a political decision: and said what were the most that would be paid to the particular church. After a few politicizes, some standard values might evolve for use in subsequent CBA studies and other decisions. The problem is wider than CBA and involves the consistency of government policy from a cost point of view. In preserving life, protecting the environment, Improving the balance of payments and saving jobs, to name only a few of the areas, economists have pointed out inconsistent values implicit in different government actions or policies.

Discounting costs and benefits

The costs and benefits of any project are likely to occur at different points in time and, thus, according to the argument in Chapter 17, will need to be discounted to their present value. If this is accepted, there remains the problem of choosing the discount rate. In practice, a public organization usually has a discount rate that it customarily uses in investment studies and will insist that this is used. However, economists often feel that this rate has been set for reasons irrelevant to the particular project or industry. In particular, in the UK, there have been standard discount rates in use for the nationalized industries during the 1960s and 1970s, but these have not been used in evaluating other government projects, nor have they been justified

Presentation of results

The crucial problem at this stage is how far the analyst's view of the project will colour the presentation of the results. From the point of view shown in Figure 19.1, we emphasize the role of the decision-maker in choosing the decision criterion and thus imply that this will determine how the results are presented. Thus the report can be expected to lead clearly to a particular conclusion or conclusions which follow from the criteria being used. Where the decision-maker has no clear criteria or does not reveal them, the report has to be very general and more of the analyst's creation.

However, there may still be problems when the decision-taker is quite clear about the decision criteria and, thus, the form of the report. These arise from the duty which analysts may feel towards the public to present rather more information than decision-takers may wish to reveal. This may be done subtly by including information in the report which is not strictly relevant to the conclusion the decision-taker reached but is relevant to other criteria. The problem will be solved differently in different countries and political systems. In the US, "whistle-blowing' and 'leaks' may occur, and in the UK, Select Committees and parliamentary questions can be used.

Thus the public sector projects involving externalities have a technique that can be used to evaluate them.

Externalities in the Private Sector

Unless the government has carefully taken over industries with significant externalities, most of the externalities will occur in the private sector. We now look at how they might be dealt with, first by the government and then by private firms.

GOVERNMENT ACTION

The government of any country has a great variety of ways to deal with externalities, and it is interesting to see how the methods vary under different political and social systems.

Public enterprise

The government can take over the activities that create substantial externalities, which has been the vowed aim of some nationalization in the UK and the US. The firm may be 'vital for national defence, such as in the case of Rolls-Royce in the UK, but its US partner, Lockheed, was aided financially by the US government rather than taken over. Similarly, both governments subsidize agriculture, which is said to have strategic importance, rather than taking it over.

One reason approaches differ is that there is no clear single criterion of which activities are necessarily those of the state. There is a theory that certain goods are public goods, but the clearest definitions of public goods say that they are:

- Non-rival - their consumption by one person does not diminish another person's consumption; and

- Non-excludable users' access to them cannot be easily restricted.

This definition leaves only a few public goods and excludes goods such as education and health care, which almost all governments provide to some of their population. Thus limiting the public sector to public goods would not satisfy many communities. Thus the extent of the public sector is essentially politically decided, although we can distinguish four kinds of public sector activity:

- Minimal public goods: police, defence, protection of clean air and water;

- Social services: education, health, social security;

- Natural monopolies: telephones, post, electricity, gas, railways, ports, television, roads, water;

- Other industries: varies from country to country.

We still have many possible government actions if we accept the idea of not taking over all industries with externalities.

Legal measures

Changes in the law can change the behaviour of private sector producers of externalities. In the simplest case, the prohibition of water or air pollution, with appropriate penalties, might prevent producing these external costs. This approach often commends itself initially but runs into two major difficulties, the definition of acceptable standards and the enforcement of these standards. Thus, governments may turn to another possibility.

Delegated legislation

This solution to the problem of externalities involves setting up some government agency that has the power to define the detailed standards required and enforce them. In its role of defining standards, it is, in effect, enacting legislation on behalf of Congress or Parliament. Thus, the Factory Inspectorate and the Mines Inspectorate enforce safety and pollution standards in the UK. The Occupational Safety and Health Administration and the Environmental Protection Agency work in similar fields in the US. The extent to which regulation of this kind should be used is a matter of lively political controversy, particularly in the US, where it has been proposed that cost-benefit studies should be undertaken to decide whether the regulations are more costly than the externalities they seek to prevent. Car safety regulations neatly illustrate the problem: would a simple law such as making seat-belt wearing compulsory be more cost-effective than the detailed requirements on car safety being developed and enforced by the EPA in the US?

Changing property rights

Another solution to externalities such as pollution is to grant those affected the right to sue the offender. This has already been done in monopoly cases in the US, where parties injured by particular monopolistic practices may obtain damages in certain circumstances. An extension to pollution and other costs might prevent some firms from taking chances. Similarly, removing the restrictions on air passengers' rights to sue for injury in the UK would internalize the cost of air safety. (Passengers on US airlines already have some rights to sue for injury, while other countries abide by the limits agreed in the Warsaw convention.) Conversely, granting property rights in external benefits to firms would allow them to charge for them. However, it isn't easy to see how this might work, as many benefits are widely diffused.

Taxes and subsidies

One way of dealing with external benefits is for the state to pay subsidies to firms that produce them. Thus in the UK, firms receive subsidies for locating in areas of high unemployment and, in some cases (aluminium smelting), for aiding the balance of payments. In both the UK and the US, firms can often obtain hidden assistance from local or state governments because they are employing in an area that is prepared to pay them for this external benefit.

Similarly, taxes on external costs could, in theory, provide the funds for the subsidies outlined above. There do not seem to be many successful examples of such taxes. However, oil depletion taxes in Norway and the UK could be considered charging the oil companies for imposing the 'externality' of less oil on future generations. Congestion taxes in large cities have often been proposed but usually meet practical and political problems; however, high parking charges could be considered a congestion tax.

Transfer payments

Governments could deal with external costs by making an income payment to the sufferers, usually called a transfer payment. Examples of this are the payments in the UK to people who are disabled, which, when the disability is caused by industrial injury, can be considered compensating them for an externality of production, for which the firm, or insurance, may not be liable. Similarly, payment for sound insulation to people living near airports or new roads is a transfer payment for externalities. In the US, some of the yields of the windfall profits tax on oil companies have been earmarked for transfer payments to those hardest hit by future oil price rises.

Regulation

The last alternative we shall consider in the government's list of ways of dealing with externalities is regulating the industry concerned. By this, we mean setting up some public bodies (in the UK, a quango such as the Traffic Commissioners, in the US, a body such as the California Public Utilities Commission) to oversee the industry's pricing and investment decisions. Thus, the regulating body would force the industry to provide services at prices that reflected the social cost and benefit balance rather than the private balance. Thus regulated bus companies and air services are required to provide uneconomic services to small communities, which would suffer if the services were withdrawn or charged for at their economic cost. In the US, utilities may be required to supply the first few units of gas and electricity at 'lifeline' rates that do not cover the supply cost so that poor consumers may have the service. In both UK and US, long-distance road freight haulage is regulated, presumably to prevent unwelcome 'externalities' or unrestrained price competition.

Summary

We can see that the government has many alternative ways to redress the externalities caused by private sector firms. Thus it seems likely that it could 'correct' many imbalances if it were politically acceptable. However, the amount involved might be very considerable, and the most 'productive' interventions in redressing externalities might not be the most productive politically! We now turn to ways in which the private sector does and might deal with the external effects of its decisions and projects.

Firms' responses

We must first distinguish two definitions of externalities, non-monetary effects and those which do not affect the firm. Firms sometimes undertake cost-benefit studies to identify the non-monetary effects of such programs as training and personnel services. Some benefits, such as increased output, can be easily given a monetary value. Still, others, such as better morale and fewer disputes or labour turnover, may be more difficult to quantify. They can, however, be dealt with, as we saw earlier in the chapter, and are not truly external. They do benefit the firm. With true externalities, there are four ways in which the firm can and does deal with them:

- relations with the government;

- cross-subsidization;

- corporate responsibility; and

- Public relations. The methods are not mutually exclusive but illuminate the kinds of approaches open to firms.

- Relations with the government

As we have seen earlier, the government will ensure that some externalities are dealt with. The firm will probably attempt to minimize the penalties for external costs and maximize the subsidies or credit for external benefits. They may, as in the US, act with other firms or independent research centres to show that some government action on external costs is expensive. In some situations, they may find it acceptable to internalize external costs, especially when they fall equally on all their competitors. In some cases, they can be used against foreign competitors, such as car emission controls in Japan and the US.

Cross-subsidization

Some firms may be able to discharge what they feel are their obligations to those who suffer from their actions by using income from other customers. Economists usually call this cross-subsidization because the 'subsidy' comes from other customers rather than the firm. Thus firms could use high profits from selling one drug to financial compensation to customers damaged by another. Alternatively, they could use marginally higher charges to all customers to pay for below-cost services to customers in rural areas. It is interesting to see how governments react to this. For example, in electricity supply, the North of Scotland Hydro Board used to have a policy of connecting virtually any customer, whatever the cost.

In contrast, the government told the England and Wales boards not to cross-subsidize. In California, the electricity companies have been told to supply initial blocks of units below cost, thus paid for partly by other customers. The extent of cross-subsidization will vary with the company's power to generate profits, its feelings about 'disadvantaged' customers, and public and governmental pressure on it.

Corporate responsibility

Some firms state that they have responsibilities that go beyond, and may conflict with, the interests of their shareholders. If firms act to help those damaged by externalities when not forced to do so, and it is not to their advantage, then we can say they accept corporate responsibility because it was first used by Berle and Means (1967). Firms may easily do this, and the extent will depend on the freedom of action of those in the firm who wish to follow this course of action. Thus, some firms use their profits to go beyond legal, contractual, or public relations necessities in dealing with external costs.

Public relations

One way of dealing with externalities has always been public relations. This can vary from claiming credit for external benefits, and disclaiming responsibility for external costs, to more obviously 'political' action by lobbying or contributing to political causes. One of the recent examples of firms trying to turn externalities into an asset has been advertising campaigns that show the public how much they benefit when the firms comply with EPA pollution controls in the US. The implication is that the firm is conferring benefits on the public by complying with the law!