Macroeconomics Exam Solutions for Revision: Supply Shocks and Growth

Looking for help with macroeconomics exams based on supply shock and growth? See our questions and their answers on the same and learn more about correctly answering your future exams. We’ve shared these solutions to give you question-answering ideas, and educate you on various concepts, too. Our company also offers economics exam help on various other topics.

Explain Shocks and Growth with a Focus on The Supply Side of Economics

Macroeconomics was developed as a framework for analyzing the transmission of aggregate demand changes through the economy. This framework has proved inadequate for handling disturbances that originate on the supply side. Traditional macroeconomic models have a production sector that has a single homogeneous output made for the most part with a single variable input; technological progress is essentially ignored. This framework is unhelpful when we need to analyze changes such as a major price rise in one of several variable inputs, or the emergence of a major new extractive industry; both these examples are highly relevant to understanding the United Kingdom over the past two decades. It is also unhelpful if we wish to understand the determinants of economic growth over the medium to long term, as opposed to short-run fluctuations in the growth rate over the business cycle. Even the real business cycle theorists, who rely on 'real' technological and taste shocks to drive the business cycle, are not able to address these major structural and long-term issues. With real business cycles, technological progress may be random, but it is still exogenous and unchanging (in the statistical sense of stationarity).

The oil price rises of 1973 and 1979, the expansion of North Sea oil production, and the worldwide productivity slowdown of the 1970s were too important to be ignored. Here, we examine the two large supply shocks that have hit the United Kingdom since the end of World War Two, consider the evidence for a productivity growth miracle in the 1980s, and examine the long-run causes of growth.

How Does The 1973 Oil Price Rise (UK) Relate to Shocks and Growth?

It is instructive to recall the way in which the 1973 oil price rise was analyzed by various commentators on the UK economy. The analysis of this section draws on Miller (1976). Remember that the problem at that time was the quadrupling of the oil price. Virtually all oil was imported.

The principal way in which the policy-makers in the United Kingdom looked at the problem seems to be through orthodox Keynesian eyes. In the context of Model I, imports are a leakage from the circular flow system so they affect the economy just like a massive increase in indirect taxes. The tax revenue, however, accrues to foreigners. A typical figure quoted for the size of this increased import bill was £1500m. A clear example of how a should see this problem is provided by G. D. N. Worswick, the Director of the National Institute, in his evidence to the Public Expenditure Committee (1974):

If nothing is done about the substantial rise in the price of oil, that figure of £1500m will be taken out of the system. There will be that much less spent in the following period and there will be a contraction of demand and a contraction of output in due course together with a contraction of employment. In this case, the rise in the price of oil has a profound contractionary effect on all countries. (p. 42)

When the government is making up its balance of the budget over the year as a whole it must allow for the fact that real consumption will be less than it would be if the price of oil had not risen. The present Chancellor has said that he wishes to have a new look at the situation later in the year. As it’s evident now, he would need to be expansionary. (p. 43)

How Does a Rise in Import Value Affect Supply Shocks and Growth?

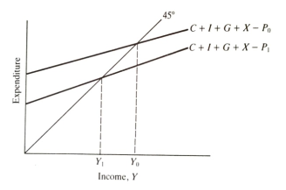

The effect of a rise in the value of imports can easily be analyzed in the context of Model I. The initial position in Figure 12.1 is with the aggregate expenditure line C+I+G+X-P0. This gives an initial level of income equal to Y0. An increase in the value of imports represents a greater "leakage' of expenditure from the circular flow, so the aggregate expenditure line falls to C+I+G+X-P, This will lead, through the downward multiplier effect, to a lower level of income Y1, We would normally expect this downward fall in income to be accompanied by an increase in unemployment. This is why the Keynesian response to the oil crisis was to point to the dangers of depression and to propose reflation.

Figure 12.1 The Keynesian analysis of the oil price rise.

Offsetting policies on the part of the government would simply involve either increasing expenditure or reducing taxes so that aggregate expenditure shifts back towards its original position. The balance of payments deficit is thus reinforced. The problem, of course, is not really as simple as that. For one thing, we have said nothing at all about inflation. More importantly in the present context, however, the concept of income is ambiguous. The simplest way to see this is to ask what would have happened if the elasticity of demand for oil had been unity. The import bill would have remained constant following the oil price rise. Does this mean that domestic income would have been unchanged? The answer is clearly no. Although there is no direct change in real GDP because physical output and the GDP deflator are unchanged, since the value of the things we produce has fallen relative to the things we buy from abroad, domestic income has unambiguously fallen in a real and more general way. What this means is that, even if there was no impact effect on unemployment, the possibilities for domestic absorption have fallen. There has to be a fall in domestic real income.

While domestic income has to fall owing to this terms-of-trade loss, it does not necessarily follow that some reflation should not be applied. Miller argues that the view at the time was that the required fall in income was less than the fall from Yo to Y, in Figure 12.1 and this is why expansionary measures were advocated. The problem with this approach, of course, is that even if it were successful in avoiding unemployment in the short run, it certainly increases inflation, which many would argue would increase unemployment even more in the long run. The outcome would appear to be consistent with this latter view. Unemployment did not rise as rapidly in the United Kingdom through 1974 and 1975 as it did in many other countries, whereas the inflationary experience was considerably worse in the United Kingdom.

Unemployment in the United Kingdom, however, continued to rise subsequently, though in many countries it started to fall after 1976, Miller concludes that while Keynesians were not unaware that there would be imported inflation', they believed that a gradual return to full employment should be possible through 'expansionary fiscal policy and permissive monetary policy'. In strict contrast to this Miller believes that the Monetarist logic predicted no inflation or recession as a consequence of the change in the terms of trade so long as fiscal and monetary policy were unchanged" (Miller, 1976, p. 509). Miller bases his analysis of the Monetarist position upon the summary of the evidence presented by Laidler to the Expenditure Committee (Laidler, 1974). However, this summary was written either by the Committee members themselves or by the Civil Service. Laidler's own evidence does not bear the interpretation Miller puts upon it (nor, in reality, does the summary).

The first point to notice about Laidler's evidence is that he is absolutely clear that 'If oil prices have gone up and the terms of trade have moved against this country, we are poorer, and it is impossible for people to protect their standards of living against that' (p. 55). Second, he answers the question about the price level by reference to an earlier point about the net effect of a decrease in indirect taxes financed by higher direct taxes, at a given level of national income. There he says, 'If there were no net decrease in purchasing power, I cannot see how ultimately the price level would be different' (p. 51). In contrast, the Director of the National Institute was reported to have argued, by analogy to an increase in indirect taxes, that inflation would rise because people would ask for and obtain higher wages to compensate for the higher oil price. Indirect taxes rising would be inflationary and more inflationary than income taxes of equal yield. To this Laidler replied:

If it is the case that people notice that indirect taxes have changed the purchasing power of their gross incomes before they notice that direct ones have done so, I cannot believe that this is any more than a very short-run phenomenon. It is one thing, in any case, to ask for a wage increase and another thing to have it granted. (p. 55)

The overwhelming impression that emerges from Laidler's evidence, in its entirety, can be expressed as two main points. First, the impact effects of the oil price rise should be clearly distinguished from the ultimate or long-run effects. Second, a clear distinction must be drawn between relative price changes and sustained inflation of the general price level. The oil price rise is a relative price change and, although it will undoubtedly raise the price index in the short run, it will only lead to a long-run rise in the price level if it is followed by monetary expansion. An appropriate framework for expounding the Monetarist analysis might be Model III.

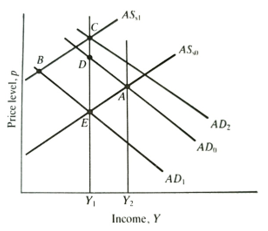

Consider the initial position at A in Figure 12.2. The short-run aggregate supply curve can be thought of as depending on the expected price level. What then is the effect of a rise in the price of imports? First notice that, although the physical production possibilities of the economy are unchanged since the relative price of domestic output has fallen, we should regard long-run aggregate supply as having fallen from Y to Y, this is the terms-of-trade loss. There are two other effects. First, there is a leftward shift of the short-run aggregate supply curve from AS to AS. This is due to the direct effect of import prices on the domestic price level plus any immediate effect on price expectations. The second effect is the Keynesian one. Aggregate domestic demand will move from AD to AD, due to the rise in the import bill. Both Monetarists and Keynesians should accept the story so far. The impact effect is a move from A to a position like B. There has been a rise in the price level and an increase in unemployment associated with a decline in domestic output. The disagreement is about the next step in the argument.

The Keynesians do not have a next step. The economy has settled into a depression at B so expansionary fiscal policies are required. Raising aggregate demand will move the economy to C, thereby eliminating unemployment. The problem with this analysis, however, is that even Ca is not a full equilibrium. This is because AS, was drawn for an expected price level somewhere between that at A and that at B. As these price level expectations are revised upwards, the short-run AS curve will shift further. If policymakers raise aggregate demand still further to avoid unemployment, this upward spiral will continue, as they found to their cost. The Monetarist analysis points to the fact that B is not a point of full equilibrium. If the monetary and fiscal pressures which are due to the authorities remain unchanged, the economy will eventually return to a point somewhere in the region of D. This I because excess supply in some markets will cause some prices to fall, so eventually short-run AS will shift back down. Also, there will be some north-eastward shift of AD due to a change in the pattern of expenditures following the increase in import prices. The ultimate effect of the oil price rise on the import bill will, ceteris paribus, be less in the long run than in the short run because expenditure patterns take time to adjust. At D the price level may be slightly higher or lower than at A, but it will not be substantially different.

Figure 12.2 The oil price rise with supply effects.

Explain Keynesian and Monetarist Analyses Weaknesses and Differences

The problem with this Monetarist analysis is that we have no information as to how long it will be before the economy returns from B to D. The problem with the Keynesian policy prescription is that it necessarily leads to a higher price level and, therefore, to faster inflation in the interim. The key difference in the analysis of the problem is that Monetarists see the economy as self-stabilizing within a reasonable time period. Keynesians recommended policies to counter the impact effects on the assumption that the economy would not be self-stabilizing with any rapidity and that the unemployment target should be given high priority.